Coast FIRE refers to when we have enough investments today that will passively grow over time in order to support our expenses in retirement.

The idea is to front-load as much of our investing as possible and then allow compound interest to work it’s magic.

This type of financial independence has seen a rise in popularity due to it being a more achievable and balanced way to become financially independent. That is because with a little work up-front, Coast FIRE can shift the burden of funding our retirement from us actively saving to compound interest passively growing.

Upon becoming Coast FIRE, we would no longer need to maintain a high savings rate and would only need to make enough money to cover our everyday expenses.

With that being said, let’s learn how to calculate your Coast FIRE number.

How do you calculate your Coast FIRE Number?

Our Coast FIRE number is the amount of investments needed to passively grow over time via compound interest without the need to continue actively saving.

In other words, if we stopped saving altogether today, what is the amount of investments needed today that can then grow into a nest egg capable of covering our expenses in retirement?

With a few simple formulas, we can easily figure this out.

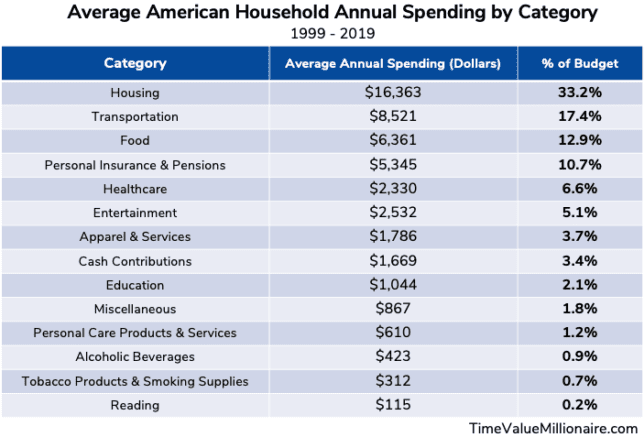

Going forward, I will be using data from the Bureau of Labor Statistics in order to calculate an example Coast FIRE number.

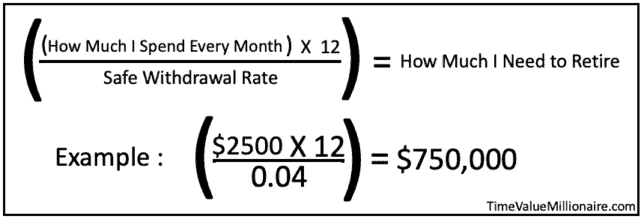

Step 1 – Calculate our Baseline FIRE Number

Our first step in order to calculate our Coast FIRE number is to first calculate how much we need to be financially independent. This is our Baseline FIRE number.

We can do this with the following formula:

Note: In this case, I am using 4% as the withdrawal rate. This is a common safe withdrawal rate to use based on research from the Trinity Study. You can adjust the withdrawal rate based on your own individual risk preferences.

Here is how the above formula works:

- Multiply our monthly essential expenses by 12 in order to give us an estimated FIRE annual budget

- Divide our estimated FIRE annual budget by our safe withdrawal rate

- The final number is the portfolio required to achieve financial independence

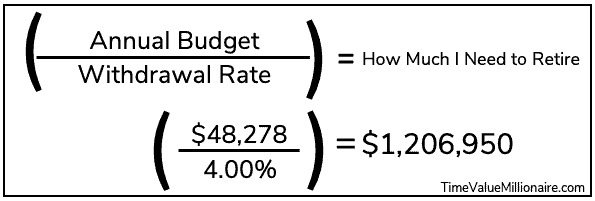

According to the Bureau of Labor Statistics, the average American household’s average annual budget from 1999 – 2019 was approximately $48,278. This will be our numerator.

Leveraging the FIRE formula from earlier, we can now calculate a potential FIRE number for the average American household (assuming a 4% safe withdrawal rate):

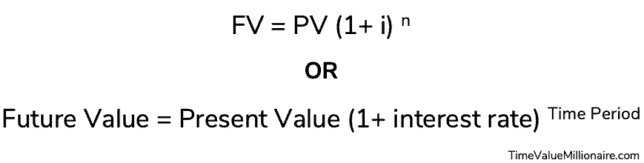

Step 2 – Calculate Coast FIRE Number using the Time Value of Money

After calculating our Baseline FIRE number, we can leverage the time value of money in order to calculate our Coast FIRE number.

The components of the time value of money are as follows:

- Future Value of Money (FV): What will my money be worth in the future?

- Present Value of Money (PV): What is my money worth today?

- Interest Rate (i): What interest is my money earning?

- Time Period (n): How long is my money being invested?

We can arrange these components into the following formula:

As a reminder, our Coast FIRE number is the amount of investments needed to passively grow over time via compound interest without the need to continue actively saving.

In other words, Present Value = Coast FIRE Number (investments needed today).

By the same token, Future Value = Baseline FIRE number (our future nest egg).

However, in order to calculate our Coast FIRE number, we need to define a time period and interest rate.

For the interest rate, we will assume that our investments mirror the historical returns of the S&P 500:

This gives us an interest rate of 7.8%.

As for the time period, we will assume that we want to achieve Coast FIRE by 35, giving our investments 30 years to grow before we decide to retire at 65.

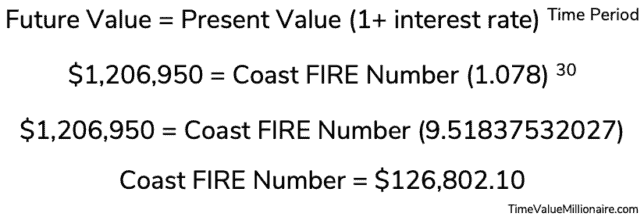

This results in us having all the variables we need:

- Future Value of Money (FV): $1,206,950

- Present Value of Money (PV): Coast FIRE Number

- Interest Rate (i): 7.8%

- Time Period (n): 30 Years

Using a Present Value Calculator, we can now solve for our Coast FIRE number:

In our fictional example above, our Coast FIRE Number would equivalent to $126,802.10.

The Pros and Cons of Coast Fire

What are the Pros of Coast FIRE?

The earlier you start, the easier it is

Compound interest is an amazing thing.

Here is a data visualization showing how powerful it can be over time:

As a result, we can see that investing earlier gives us two major advantages:

- More time for compound interest to work for us

- Less money required to achieve financial independence

The longer we put off investing, the less of an impact that compound interest will have.

You have a lot more flexibility

Don’t be a slave to the golden handcuffs.

With our future retirement already funded, we have the flexibility to work on our terms.

If we don’t want to continue working a high-paying/high-stress job, we don’t have to. We can instead become time millionaires and do less-stressful and/or more meaningful work that can support our lifestyles.

What are the Cons of Coast FIRE?

You still have to work to support yourself

The major drawback of fully embracing a Coast FIRE lifestyle is the fact that we still have to work in order to support our everyday expenses.

However, if you are apart of the antiwork movement and just hate the idea of working, there are several things you can do:

- Increase your passive income streams that can make support your current lifestyle

- Keep your big 3 expenses to a minimum

Past returns aren’t indicative of the future

When calculating our Coast FIRE number earlier, we assumed an average investment return of 7.8%.

However, past returns are not indicative of what will happen in the future.

Instead, we should always err on the side of caution and assume more worst-case scenarios. This can help us avoid not having a full-funded retirement at whatever age we decide to retire at.

Final Thoughts

Earlier this year, Mrs. TVM and I achieved Coast FIRE.

Instead of quitting our current jobs, we decided to take advantage of our Coast FIRE status.

More specifically, with our first child being due in Q1 2022, our plan is for Mrs. TVM to take additional time off work in order to be with them (her company doesn’t offer maternity leave).

Will this will impact our savings rate? Sure, but life is more than just about money.

We are thankful for the financial flexibility in order to live our lives more on our terms.

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.