“If you learn only one thing from this class, let it be the time value of money.”

That statement was made by my Business Finance Professor on Day 1 and ended up being the most important class I took while getting my Bachelor of Science in Finance.

In fact, that class ended up being the most important class that I have ever taken.

That is because I was introduced to concept of the time value of money.

What is the Time Value of Money?

The time value of money is the concept that money is more valuable today versus an identical sum in the future.

There are three primary reasons for this:

- Money invested today has the ability to earn interest over time

- Inflation can decrease purchasing power of money in the future

- Potential risks with not receiving the money in the future, so it’s better to receive it today

Factors affecting the Time Value of Money

The components of the time value of money are:

- Future Value of Money (FV): What will my money be worth in the future?

- Present Value of Money (PV): What is my money worth today?

- Interest Rate (i): What interest is my money earning?

- Time Period (n): How long is my money being invested?

When making any financial decision, it is important to consider each one of these variables together.

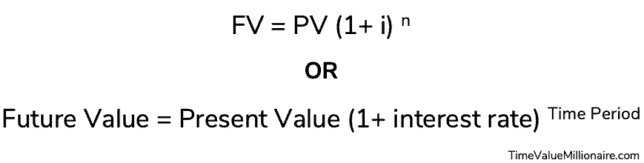

We can do this by compiling them into the following formula:

Using this formula, let’s look at a basic example:

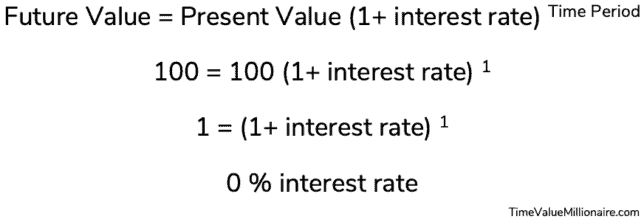

Imagine someone offered you $100 today or $100 one year from now.

Which option should you choose?

Because the money’s present value and future value are identical, you should take the $100 today.

That is because the $100 today has an opportunity to earn interest over the next year.

If you accepted the $100 today and invested it in a mutual fund that earned 7% over the next year, your $100 today would now be worth $107 a year from now.

Contrast that with receiving $100 a year from now which would be equivalent to receiving a 0% interest rate.

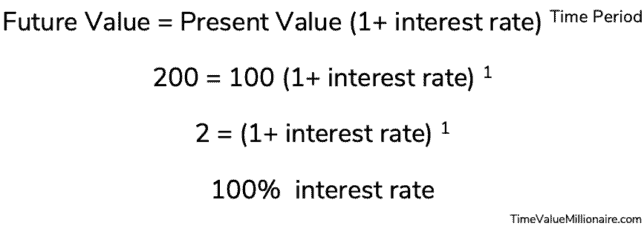

However, what if our kind Samaritan revised their offer to giving you $100 today or $200 one year from now? Which option do you choose then?

In this case, you would be better off taking the $200 one year from now. When comparing the future value of $200 to the present value of $100, we can calculate this to being equivalent to receiving 100% in interest in one year. That’s a pretty damn good return on investment!

Importance of the Time Value of Money in Daily Life

When it comes to everyday financial decision making, we can begin to see the importance of the time value of money.

Let’s look at some real life examples.

Loan Repayment

According to a study by Pew Charitable Trusts, 8 in 10 Americans carry some form debt.

That debt includes but is not limited to: mortgages, car loans, student loans & credit cards.

You may be inclined to pay off that debt as soon as possible.

However, that approach may not make the most financial sense.

Let me explain with an example from my life.

In 2020, Mrs. TVM and I were fortunate enough to buy a home. We have a 30 year mortgage with a fixed interest rate of 3.5%.

Should I make extra payments and pay off my mortgage as soon as possible?

According to the time value of money, the answer would be no.

I can instead invest that extra money in order to earn an average of 10.2% from the stock market vs paying the 3.5% interest associated with my mortgage.

In this case, our money can earn 6.7% more by investing in the stock market.

However, what if I had a credit card that had a 25% interest rate? In this case, that 25% interest rate is far greater than the 10.2% I could potentially earn in the stock market.

I would therefore realize a 14.8% greater benefit by paying down that credit card balance.

While being debt free is an amazing goal, there are some cases where it doesn’t make sense to pay it off as soon as possible.

Financial Independence

Investing in order to reach financial independence is the most common application of the time value of money.

By investing today, your money can earn interest over time and be worth more in the future.

The first step is calculating the future value of money that you need – this is also commonly referred to as your Financial Independence (FI) Number.

If want to know how to calculate your FI number, I wrote a post on How to Start Your Path to Financial Independence.

After calculating your FI Number, you can then calculate how long it will take to become financially independent. This can be done using the time value of money formula in order to evaluate how your current portfolio’s present value will grow via different interest rates.

Bonus: Winning the Lottery

If you are fortunate enough to win the lottery one day, you will have two payout options: annuity payments or lump sum.

According to the time value of money, your ideal situation would be to take the lump sum.

That is because the larger lump sum can be immediately invested and begin earning interest.

At the end of the day, the interest earned by the lump sum will be more than the interest accrued by the annuity payments.

To illustrate this, let’s look at a data visualization.

Assumptions:

- I theoretically win $20,000,000 in the Mega Millions

- I live in FL and which doesn’t have a lottery tax

- Annuity Payout: $455,928 / year

- Lump Sum: $9,485,928 / one time

- We invest our winnings in an S&P 500 mutual fund earning 10.2%

Final Thoughts

The time value of money provides the foundation for every financial decision that we make.

Aside from optimizing our finances, the time value of money was also a major influence on the name and mission for this website. We even share the same TVM acronym 😉

Have you ever made a major financial decision using the time value of money?

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered to be advice, research or an invitation to buy or sell any securities, please see my Terms & Conditions page for a full disclaimer.