There is one thing that motivates me to achieve my goals: seeing progress.

However before we can see progress, we first need to understand what our exact goal is.

This is especially true when it comes to financial independence.

So today we will be examining how to calculate how much money is needed to be financially independent as well as how to calculate our progress to financial independence.

Step 1 – Record Your Monthly Expenses

The first step in determining how much we will need in order to achieve financial independence is to have a clear understanding of what our monthly expenses are.

This can be done by recording your expenses for 3-6 months and then taking an average.

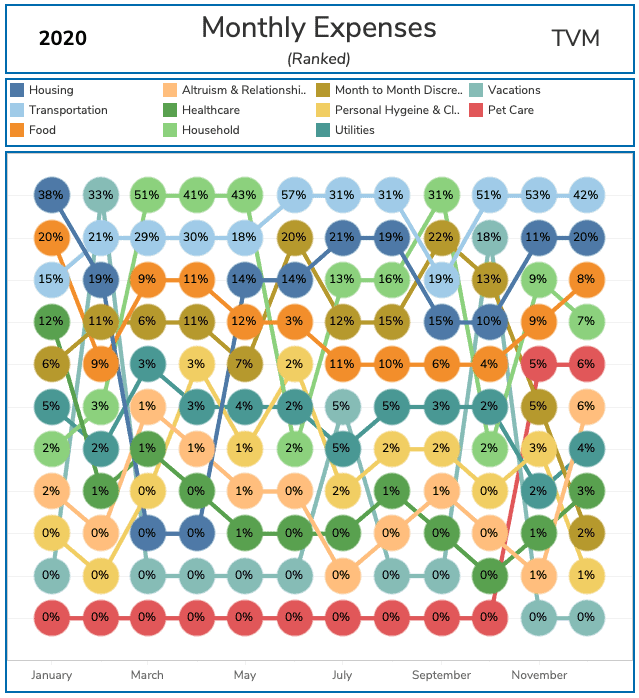

Calculating an average is important because it can account for fluctuations in your monthly spending. It will capture your everyday expenses (housing, food) as well as possible one-offs (vacations, a broken down car).

Looking at my own data below, you can see a spike in my vacation category in February and July. If I just used data from March, April, May… I would not have captured that in my average monthly spending.

Depending on how OCD you are, you can track your expenses manually by using a spreadsheet or via an automated expense tracker like Mint or Personal Capital.

Step 2 – Decide on a Safe Withdrawal Rate

The second step in calculating our FI number is to decide what safe withdrawal rate to use. It is also sometimes referred to as the sustainable withdrawal rate.

Fidelity defines a safe withdrawal rate as “the estimated percentage of savings you’re able to withdraw each year throughout retirement without running out of money.”

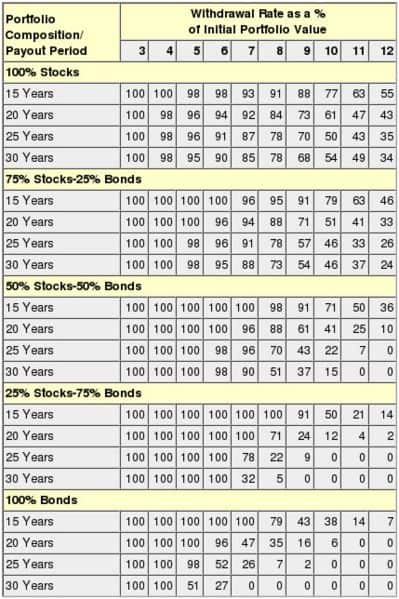

However, what percentage should we use? We can answer this question by looking at the Trinity Study, which published the following results:

We can see from the table above that a safe withdrawal rate of 3 – 4% provides the greatest probability of never running out of money.

Step 3 – Calculate Your FI Baseline Portfolio

Now that we have both variables in the FI equation defined, we can calculate a FI Baseline Portfolio.

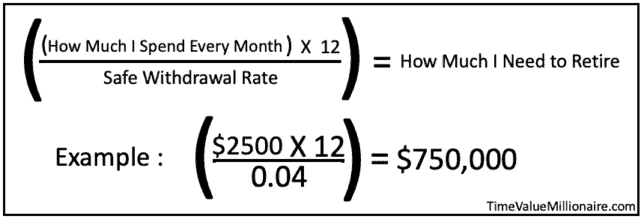

This can be done using the below formula:

In our above example, an individual that spends $2500/month on average and uses a 4% safe withdrawal rate will require a portfolio of $750,000 to reach Financial Independence.

However, that isn’t the end of the story.

That $750,000 portfolio is based on that individual’s current spending levels today. If they anticipate spending more or less in the future, then the FI Baseline Portfolio will need to be adjusted to reflect their anticipated monthly expenses.

If you are like me and want to maintain a lifestyle similar to what you are living today, then your FI Baseline Portfolio is a good target to measure yourself against.

Step 4 – Calculate Your Progress to Financial Independence

Steps 1-3 establish a clear goal to financial independence.

Now we can begin to measure our progress to financial independence.

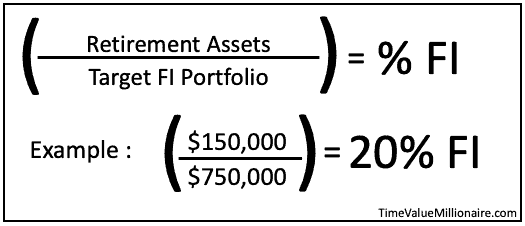

This can be done using the formula below:

It is important to only include investments that you plan to draw from in retirement in the numerator. This may be different then your net worth.

This can include but is not limited to:

- IRAs

- 401(k)s

- HSAs

- Traditional brokerage accounts

After you do this calculation, you may find that your % FI is much lower then what you thought.

As a result, you may feel overwhelmed and discouraged.

I understand that feeling because that’s exactly how I felt when I started. So I developed a system to help me stay motivated.

As a Project Manager, whenever I’m assigned a new project, one of the first things that I do is break the project up into individual milestones. This helps with organizing what progress needs to be made by specific points in time.

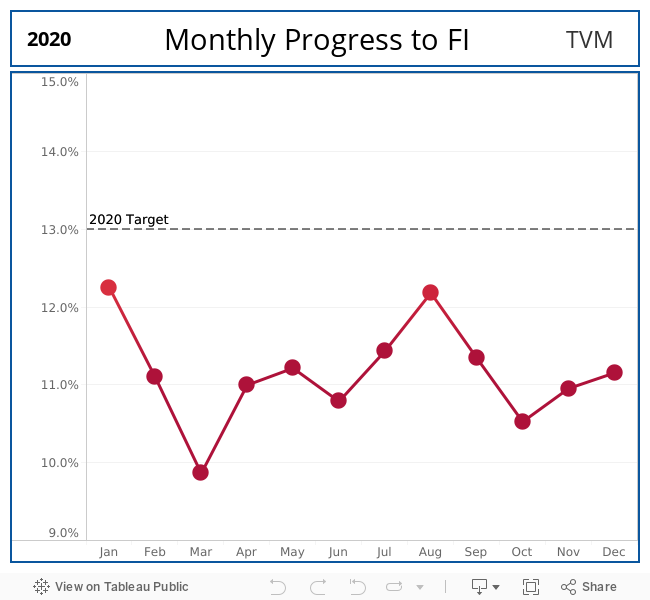

Instead of looking at my journey to financial independence as a whole, I instead look at progress to financial independence year by year.

At the beginning of every year, I set a % FI goal based on where I want to be by the end of the year and focus on that goal.

This has given me a greater sense of satisfaction with the progress that I am making.

Step 5 – Repeat, Rebalance, Rebaseline

Shit happens, circumstances change.

The plans that you originally had when you first started may very well change over the years.

And that is okay.

As our life situations change, we may need to go back to the drawing board and make sure our FIRE strategy is aligned with our new goals. This could also include calculating a new baseline portfolio based on expected changes in our monthly expenses.

Four years ago, my original FIRE plans included moving to Hawaii (a high cost of living area) which meant needing a bigger target portfolio. However, I have since adjusted my plans to not move so I can become financially independent sooner.

Make it a point to actively revisit your FIRE strategy every 6-12 months and ensure that it is still aligned with your life goals. Repeat, rebalance and rebaseline as necessary.

Final Thoughts

If we don’t have a clear understanding of what our goals are, how can we expect to see any progress?

And without seeing progress, how can we stay motivated to meet our goals?

Unless your Michael Scott.

How do you measure your progress to financial independence? Let me know!

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.

Love the blog TMV! I really like the graphics and formulas you use. I can tell you love data as much as I do. And you clearly have your goals defined. We are well on our way to early retirement! Keep up the great work Matt!

I appreciate it FLA! My favorite graphic was obviously Michael Scott, really drives the message home 😉 Once we clearly define our goals, it definitely makes the progress much easier to see. Thank you for your kind words, we are both definitely on the right path! 🙂