The path to retirement can be defined by the following equation:

Work X years in order to save Y dollars to retire at Z years old.

Traditionally speaking, this equation has been built on the assumption that we are only able to do this through earning an active income; a fancy term referring to income received for performing a job.

While most of us earn an active income via a day job, active income has several downsides:

- You are actively trading your time for money

- Your income is limited by the number of hours that you work

- You have to work a job that you may not like

- Your savings rate can only be influenced by cutting your budget, leading to potential deprivation

- You are not in control of your income’s growth

However, I want to focus on the fifth bullet.

If we are unable to grow our active income, then this will further amplify the other disadvantages listed above.

With that being said, is wage growth really a problem in the United States?

Using data from the Bureau of Labor Statistics and Federal Reserve Bank of St. Louis, I created the following data visualization mapping the average wage growth in the United States alongside personal savings rate data as well.

Even though the average savings rate / hour is not great, the average hourly wage has grown a lot!

However, that data is not adjusted for inflation.

Let’s see how the visualization will look once we adjust our figures into January 2021 dollars:

As you can see, the average hourly wage in the United States has remained largely unchanged since 1964.

This tells us is that average wage growth in the United States has been virtually non-existent due to inflation.

So if our active income is not keeping up with inflation, how can we expect to retire early without getting burnt out along the way?

Fortunately, there is another category of income without these constraints.

It is called passive income.

What is passive income?

Formally, Wikipedia defines passive income as “money that you earn from assets that you own that doesn’t consistently require active input.”

Informally, I like to define it as “money that you earn while you are sleeping.”

Some examples of passive income include:

- Dividends from Stocks

- Rent from Rental Properties

- Ad Revenue from Websites

- Selling Digital Products

- Credit Card Rewards

How can passive income help you retire early?

Earning passive income takes some active and upfront involvement to initially set up.

However, passive income has two mathematical advantages that completely change the retirement equation that we saw earlier.

First, passive income has the ability to scale exponentially.

Because active income is largely a function of time, earnings are limited to the number of hours that you work.

This is in contrast to passive income, where time does not have the same impact on potential earnings.

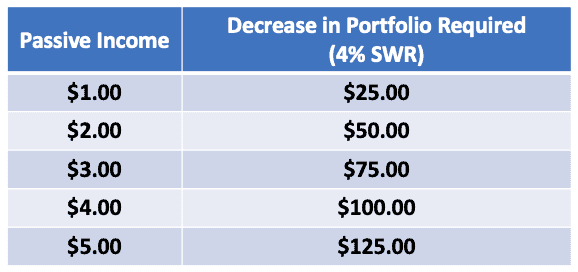

The second advantage is that earning $1 in passive income is equivalent to saving $25 for retirement.

The idea is that if you have recurring passive income that can cover recurring expenses, this would result in a smaller retirement portfolio needed in order to cover the rest of your living expenses. This is based on the same math behind the 4% rule developed by the trinity study.

To drive the point home, let’s go through a situation.

Suppose that Dominick makes the federal minimum wage of $7.25.

If we average the U.S. personal savings rate from the last 57 years (Jan 1964 – Oct 2020) that would mean he would only be saving 8.8% of his income for retirement or roughly $0.64 an hour. This would result in Dominick needing to work 39 hours in order to save $25 for retirement.

However, let’s say that Dominick was able to generate $1 in passive income. That $1 in passive income would be the equivalent of now not having to work 39 hours in order to generate the same impact to his retirement portfolio.

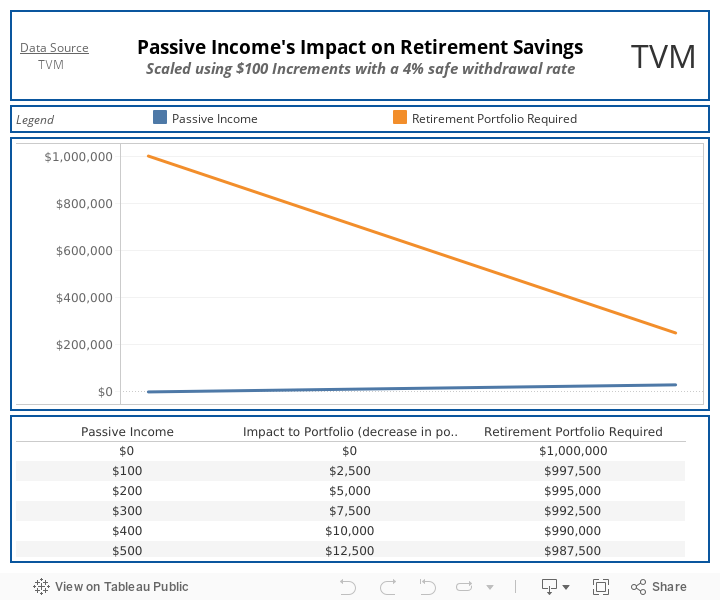

Let’s now see how larger amounts of passive income can impact the journey to early retirement:

The portfolio required for retirement decreases substantially with minimal increases in passive income.

As an example, developing a passive income stream of $10,000 / year would result in needing $250,000 less in retirement savings (scroll through the table for more details).

This literally equates to saving years off a journey to early retirement.

Final Thoughts

Creating true passive income is not an easy task – usually requiring an upfront investment of time and/or money.

However, if you are willing to invest the time in order to create passive income streams, they can provide a greater impact on your journey to an early retirement vs solely relying on an active income.

Do you have any forms of passive income? How does passive income fit into your overall retirement strategy?

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.