Welcome to the first TVM Financial Update of 2022.

The purpose of these quarterly financial updates is to crunch the numbers, visualize the data and share our progress towards becoming financially independent.

For a recap of what happened in 2021, you can find those updates here:

- TVM Financial Update – Q1 2021

- TVM Financial Update – Q2 2021

- TVM Financial Update – Q3 2021

- TVM 2021 Annual Report

With that being said, let’s see what happened during the first quarter of 2022.

Life Update

From a life perspective, the last three months have been INSANE.

Here are some of the highlights:

We are officially parents! It’s official, Mrs. TVM and I welcomed our first child into the world. Other than some slight adjustments to our sleep schedule, getting her acclimated into the family has been fairly smooth 🙂

I published 11 posts to Time Value Millionaire. Between a stay-cation at the beginning of the year and paternity leave, I have been able to squeeze in time to publish 11 posts! I wanted to get ahead and publish a few extra posts in the beginning of the year in anticipation of the new parenting gig 🙂

Making some progress on the money pit, I mean, house. After 9 months, we finally got our new windows! You know you are old when you have friends over and say “Hey, look at these new windows… prettttyyy cool huh? Yea, they are impact resistant… no big deal.” We also ordered new siding for the house and that should be here in the next few months… which like the windows, will be pretty cool 😉

Financial Update

A couple notes:

- The data visualizations are interactive; hover over sections of the graphs for more detailed information.

- Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.

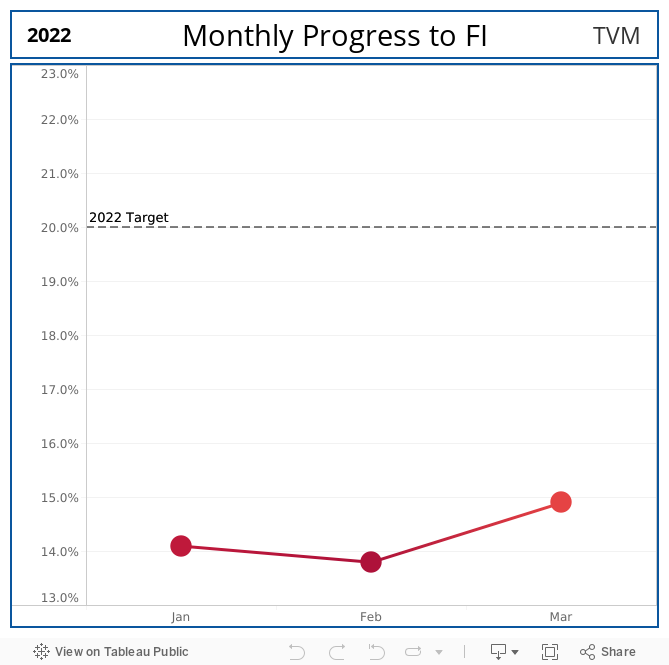

Progress to Financial Independence

From Q4 2021 to Q1 2022, our % FI decreased 0.1% from 15.0% to 14.9%.

To be honest, between the market volatility & our heavy spending in February, I’m actually surprised our % FI wasn’t lower.

As a reminder, our % FI is a function of two variables:

- Our average monthly spending

- The total balance of our FI Assets.

From a spending perspective, we do anticipate at least one more ‘heavy spending’ month at some point this year associated with some major home improvements. With that being said, pending any emergencies, we anticipate our spending to stay within it’s normal range for the rest of the year.

From a FI Assets perspective, there’s really nothing we can do beyond continuing to save 🙂

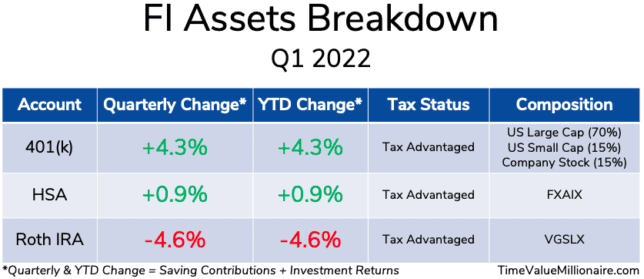

Asset Breakdown

The above table is a breakdown of our current FI Assets.

While we don’t share actual dollar figures, I will say that our total FI Assets have reached an all-time high…so that’s pretty cool I guess 😛

However, it’s still early in the year. We are just happy to see that there’s not a lot of red 🙂

Oh wait…

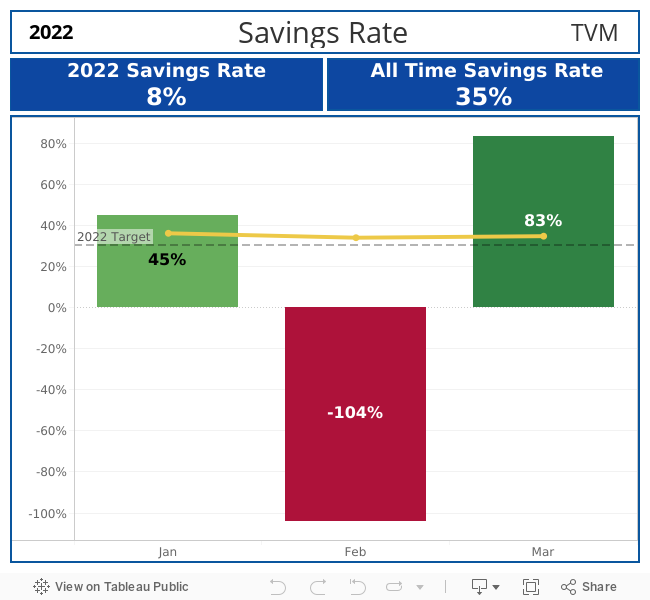

Savings Rate

Our 2022 savings rate is currently at 8%.

Considering that our savings rate was -1% in Q1 2021, I guess that’s an improvement? 😛

While we are happy with January, we SMASHED our savings goal in March!

Although to be honest, March was sort of an outlier:

- March was one of those “3 Paycheck Months” where we both received additional paychecks (happens twice a year for those who are paid bi-weekly)

- I received a bonus @ work

- When refinancing our home, we accidentally made two payments for our flood insurance, so we got that money back… woop woop!

- As part of the home refinance, we didn’t have a mortgage payment 🙂

Yea that’s cool and all, but WTF happened in February? Care to explain?

Well, let’s take a look at our monthly expenses to find out.

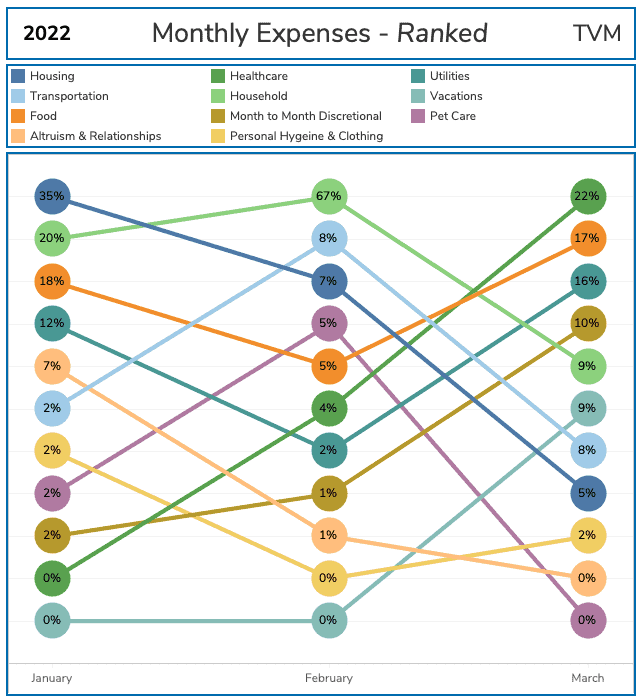

Monthly Expenses

Let’s take a look at our Expense Sankey, aka Mrs. TVM’s favorite data visualization.

The above graphic visualizes how our monthly expenses rank month over month. The percentages in the individual bubbles represent our % spending for each category for that month.

Here are some of the major spending highlights from this quarter:

- January

- Increased spending in the Housing Category was a result of:

- We had to pay some fees associated with our cash-out refinance.

- Increased spending in the Household Category was a result of:

- We bought a lot of little random things for the baby (totes, sheets, etc.).

- Increased spending in the Housing Category was a result of:

- February

- Increased spending in the Healthcare Category was a result of:

- We paid the hospital delivery fee in advance.

- Few doctor visits here and there.

- Increased spending in the Transportation Category was a result of:

- Car insurance was due again…

- Increased spending in the Household Category was a result of:

- BAM! We made the final payment on our new windows.

- We also put a down payment for new siding for our home. Definitely was not cheap… but hey, that’s the life of a homeowner!

- Increased spending in the Pet Care Category was a result of:

- The TVM Pup had his yearly physical along with some yearly tests/vaccines.

- We also went ahead and bought a 6 month supply of his flea medication in advance.

- Increased spending in the Healthcare Category was a result of:

- March

- Decreased spending in the Housing Category was a result of:

- No mortgage!

- We had to pay those pesky HOA quarterly fees though…

- Increased spending in the Healthcare Category was a result of:

- I guess when you are 27, that’s when your body starts to fall apart?

- I saw a chiropractor for the first time in my life, went to the doctor a few times… all that jazz.

- Decreased spending in the Household Category was a result of:

- After a crazy February, things went back down to normal.

- Increased spending in the Month to Month Category was a result of:

- I used a small amount of my bonus from work to buy two more trees for the orchard: a cinnamon & jabuticaba tree. Considering it took me 2 years to find a cinnamon tree, I was pretty stoked 🙂

- Despite being a self-proclaimed minimalist… I bought something that is completely unnecessary but have been eyeing for awhile. I’ll reveal what it is in my Q2 2022 TVM Financial Update when it comes in 🙂

- Vacations

- We booked another concert! We found out that the Red Hot Chili Peppers are going to be in Florida for their 2022 World Tour! This is a bucket list item for me, so I’m pretty excited 🙂

- Decreased spending in the Housing Category was a result of:

Home Value vs. Mortgage Balance

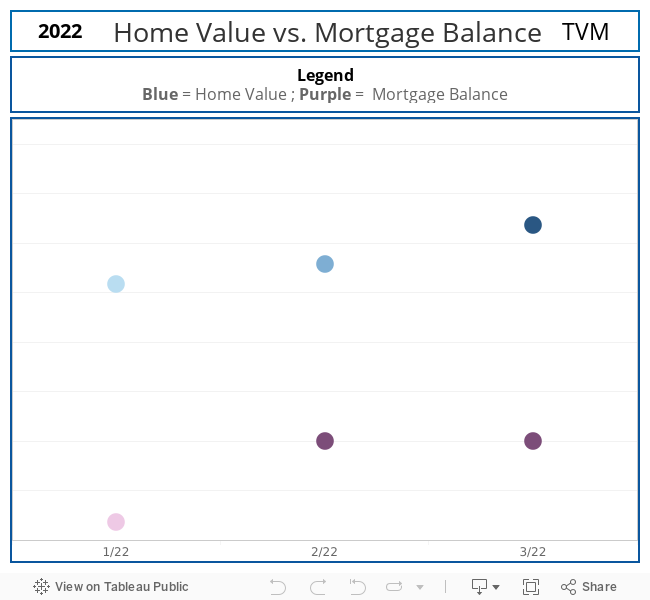

The limited supply of housing and high demand in our area continues to drive our home value higher.

Since we bought our home two years ago, it has appreciated by more than 50%. Bonkers.

Because we plan on staying in this home long-term, we executed a cash-out refinance in February. We will be using the money to make some much-needed repairs to beef up the home’s exterior.

Let’s hope we can finish these repairs before hurricane season starts in 61 days :O

Final Thoughts

From a life perspective, Mrs. TVM & I achieved an exciting milestone… We are parents now!

We are beyond blessed that everything went according to plan. Even as I look over and see her and the TVM Pup sleeping beside me, it still doesn’t feel real. It’s truly a dream come true.

From a financial perspective, meh… we still got 9 more months 😛

Thank you for reading 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.

Congrats on being parents! Life will change and hold on for the ride. Ha ha.

It is interesting seeing your financial updates. Looking back, we never did budgeting and graphing our net worth. I understand why you and other bloggers do it though for showing readers your progress to FI. We always invested, careful with spending, and paid off house early. Now being in our early 50s, I wish we had the numbers from way back when to see the progress that we made over the years.

It kind of goes to show many paths and tools to use for FI. Like part of your site name, you have time. That is the key.

Congrats again on the baby!

It still doesn’t feel real yet, except when she cries at 1 AM, 2 AM, 3:30 AM, 5 AM… 😛

Doing these financial updates help with holding ourselves accountable to our goals. It’s one thing to say you want to retire early, but another to keep yourself accountable via data/metrics that don’t lie 🙂