Welcome to the first financial update of 2021.

The purpose of these quarterly financial updates is to crunch the numbers, visualize the data and share our progress towards becoming financially independent.

Let’s see what happened during the first quarter of 2021 🙂

Life Update

Highlights

I got promoted! After being in the same position for almost 3 years, I began not feeling challenged enough. So, I interviewed internally with another department and received a call back within an hour with an offer! After leveraging my pawn stars negotiation skills, I haggled for a promotion as well as a 25% raise!

Mrs. TVM and I have adjusted to our new puppy. In my 2020 Annual Report, I announced that Mrs. TVM & I became fur parents to a golden retriever puppy. While he is adorable AF, there was definitely an adjustment period. The first month consisted of many sleepless nights getting him adjusted to his new home. As of this writing, he is finally sleeping through the entire night!

We have been homeowners for 1 year! This last March marked one full calendar year in our home! In the beginning, it felt like we were living a real life adaption of Money Pit. This was due to the previous owner neglecting basic maintenance that resulted in issues needing our immediate attention. However, things have settled down and we with are finally beginning to pivot to the “fun projects”. 🙂

Habits

In my 2020 Annual Report, I mentioned that I planned to simplify my life in 2021. To accomplish this, I decided to narrow my focus to practicing four habits, daily and consistently:

- Reading

- Writing

- Meditating

- Exercising

Borrowing inspiration from my friend Zach @ FourPillarFreedom, I decided to leverage his dead simple way of managing habits.

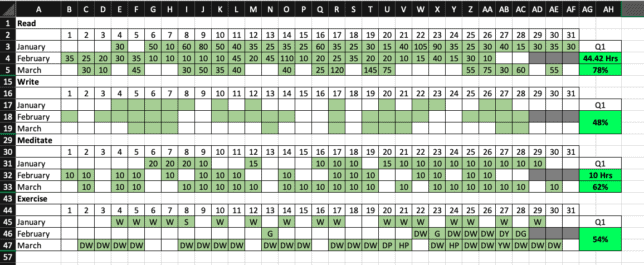

Here is how the first 90 days of 2021 looked:

What went well?

I was happy to see that I both read and meditated for over 60% of the days in Q1.

This resulted in:

- 44.5 hours of reading that lead me to finishing Clash of Kings (Book II in GOT Series)

- 10 hours of mindfulness meditation that has begun to have a calming effect on my mind

What could have been done better?

While I was near the 50% mark with my writing and exercising habits, I would like to see them closer to the 60% – 70% threshold. After some reflection, I believe I can accomplish this with the following:

- I tend to not write on days that I work extra hours in the office because by the time I get home, I am mentally exhausted. I need to do a better job at saying no so I can have the mental energy to write.

- I still don’t feel comfortable going to the gym due to COVID. Therefore, I have been actually been taking more long walks outside, especially with the pup. With him now being fully vaccinated, I plan to go on walks with him everyday if possible.

Financial Update

Time to talk money.

A couple notes:

- The data visualizations are interactive; hover over sections of the graphs for more detailed information.

- Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.

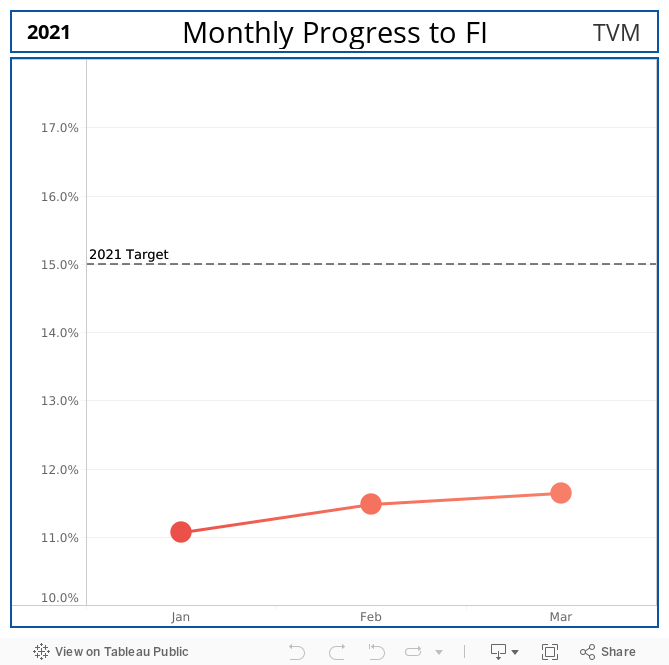

Progress to Financial Independence

Our overall % FI increased from 11.2% (Dec 2020) to 11.6% by the end of Q1 2021.

If this growth seems low, that’s because it is.

In order to hit our year end goal of 15% FI, that would require our % FI needing to increase by at least 0.3% every month. Some quick arithmetic reveals that we are 0.6% “off schedule.”

However, we actually anticipated this slow start.

While our FI Assets have grown, our significant spending in a few select categories has dragged our overall progress down.

However, this significant cash outflow will not be a problem in Q2 🙂 (read on for more details).

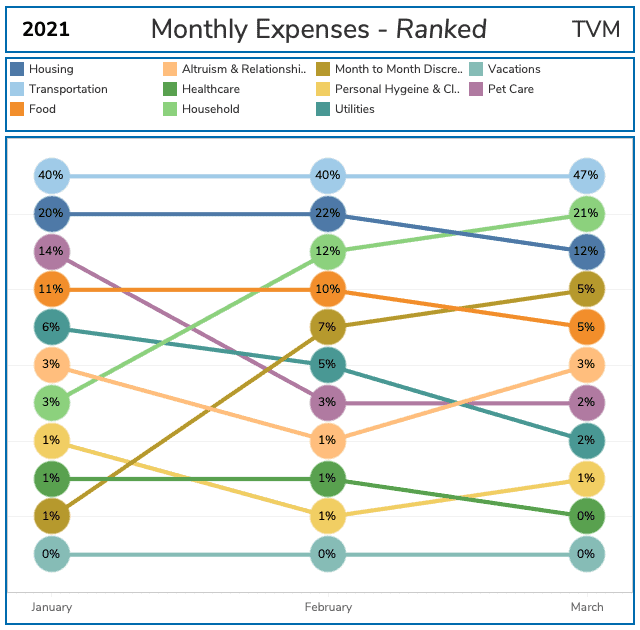

Monthly Expenses

Let’s take a look at our Expense Sankey, aka Mrs. TVM’s favorite data visualization.

The above graphic visualizes how our monthly expenses rank month over month. The percentages in the individual bubbles represent what percentage of our income was spent on that category for that month.

Earlier, I mentioned that we had significant spending in a few select categories.

Back in 2020, we made the strategic decision to dramatically decrease our savings rate in order to pay off our two auto loans ASAP.

Despite it being a strategic decision, it blows my mind that we have been spending 2 – 4 times more money on our remaining auto loan versus our mortgage. Can you tell that we want that auto loan to die?

Aside from transportation, I was curious to see how the Pet Care category was going to look after 3 months with our new puppy.

The first few months consisted of taking him to the vet every other week to get his vaccinations which added up. Fortunately, a lot of those preliminary visits are over and that category is now consisting of food and basic spoiling 🙂

Finally, our household expenses jumped in March. This was because we had a handyman come out to knock out some big projects that we didn’t have the time to do.

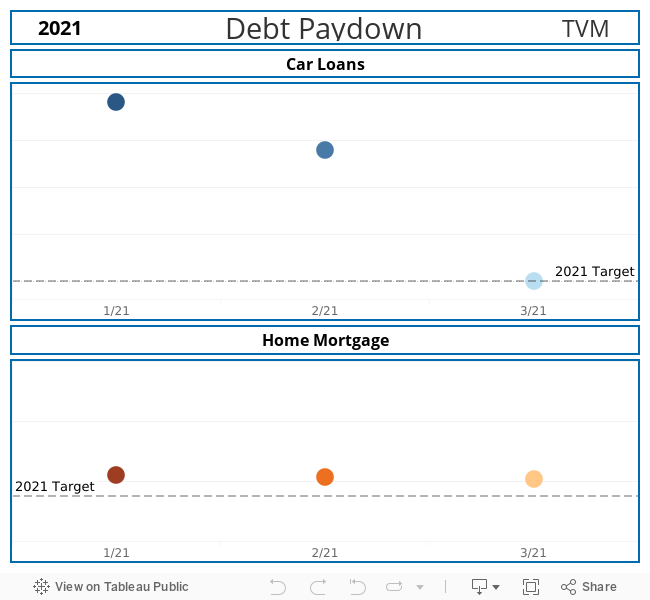

Debt Pay down

I’ll just jump right into it:

WE PAID OFF OUR SECOND AUTO LOAN 3 MONTHS AHEAD OF SCHEDULE!

Aside from our mortgage, this means that we are now completely debt free!

In all seriousness, it felt good to finally be consumer-debt free again.

This was a big milestone not only because we erased this monthly cash outflow, but we are now able to ramp up our savings rate again! This will hopefully put us back on track to hit our 15% FI goal for this year.

For those wondering why we even had auto loans:

- Mrs. TVM had an existing auto loan before we got married

- Back in Aug 2019, I got in an auto accident that completely totaled my car and I didn’t have the cash to pay for another car without a loan

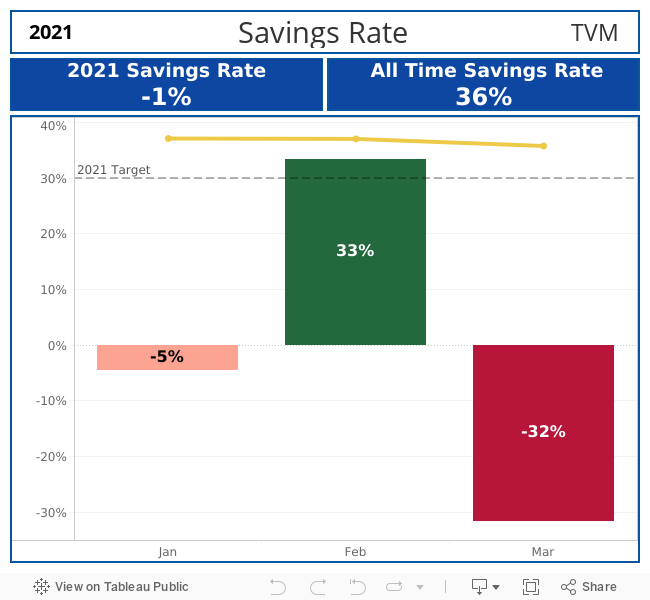

Savings Rate

Our average savings rate for 2021 is currently at -1%.

I knew we spent some serious dough, but Doh that’s a lot of red!

There were three main cost drivers that contributed heavily to the red:

- Paying off our final auto loan

- TVM pup’s preliminary vet visits

- Handyman projects

Aside from those big three items, our overall spending was more or less normal.

With the car loan out of the picture along with my promotion, we plan on significantly ramping up my savings rate to our FI Assets. So hopefully you’ll never see another negative quarterly savings rate ever again 🙂

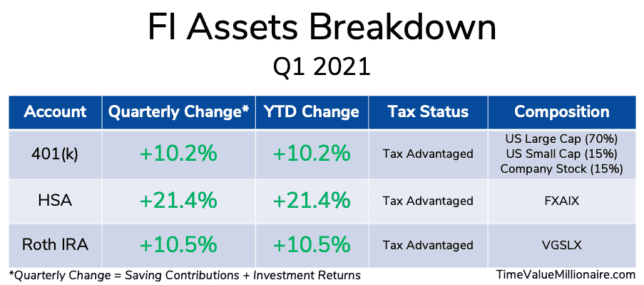

Asset Breakdown

The above table is a breakdown of our current FI Assets.

While we are happy with the overall growth from these tax advantaged accounts, we are looking forward to seeing the impact of ramping up our savings rate into these investment accounts in Q2.

Finally, I wanted to mention that while they aren’t listed here (for security reasons), we also ended up investing some spare cash into a few different cryptocurrencies.

We still believe that index funding investing is the best way to go, however we did want some exposure into this section of the market that aren’t necessarily being captured by index funds.

While we personally believe that blockchain technology will have a huge impact on the future of the banking system, as rationale investors we can’t get ourselves to put all our eggs in one basket.

Final Thoughts

From a life perspective, the first 90 days of the year ended up being pretty solid.

Actively simplifying my life by focusing on four daily habits have resulted in progress in areas of my life that I’ve wanted to grow in for awhile now. Also, the unplanned promotion and integrating the TVM pup into our lives have made life a little more interesting.

From a financial perspective, there was definitely a slow start to the year.

However, I anticipate that being consumer-debt free coupled with my salary increase will get us back on track to hitting our 2021 goals.

How has 2021 been treating you so far?

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.