Prior to switching my college major to Finance, I didn’t know sh*t about money.

Despite the importance of personal finance, only 17 states guarantee [at least] one semester of a personal finance course to all high schoolers. This lack of formal education can have severe consequences, including young adults learning critical personal finance skills from untrustworthy sources.

As a result, this article will be going over 6 essential personal finance calculations that we can use in order to help us achieve our financial goals.

With that being said, let’s dive in!

Affiliate Disclosure: Some of the links below are affiliate links, meaning at no additional cost to you, I will earn a commission if you click through and make a purchase. Please read my disclaimer for more information.

1. Net Income

Net income is also known as “take-home pay.”

This is the income that one receives AFTER subtracting taxes and other deductions including items such as insurance & retirement contributions.

The formula for net income is:

From a budgeting perspective, we should be looking at our net income vs. our gross income.

That is because while one’s gross income (compensation without any deductions) can be identical from state to state, net income can vary greatly.

As an example, here is what a 6 figure salary gets you ($100K) in California vs Florida:

| State | Gross Annual Salary | Post Tax Annual Salary | Monthly Pay | Bi-Weekly Pay | Hourly Pay |

|---|---|---|---|---|---|

| California | $100,000.00 | $67,476.24 | $5,190.48 | $2,595.24 | $32.44 |

| Florida | $100,000.00 | $75,277.02 | $5,790.54 | $2,895.27 | $36.19 |

One of the best tools in order to approximate our net income is ADP’s Salary Paycheck Calculator.

By inputting our state/county specific information, we can get an approximation of how much money we are actually bringing in.

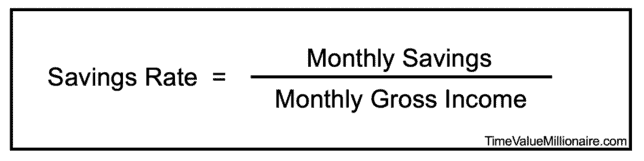

2. Savings Rate

Savings rate is the percentage of money that we are able to save on a monthly basis.

The formula for savings rate is:

A common question when calculating savings rate is why use gross vs. net income?

While one can use net income, it’s important to be aware of the mathematical implications.

More specifically, using net income in the denominator will always result in a higher savings rate. That is because if someone includes large contributions to a pre-tax retirement account (money that is being saved, but not taken out of the net income received) it will artificially inflate how much we are actually saving.

And while using gross income will result in a more conservative savings rate, it is closer to reality. From a retirement planning perspective, it’s better to be more conservative in our assumptions.

This is important because our savings rate is the most important metric to track when it comes to financial independence. For more information, I recommend checking our Mr. Money Mustache’s “Shockingly Simple Math Behind Early Retirement,” detailing exactly how different saving rates impact how soon we are able to retire.

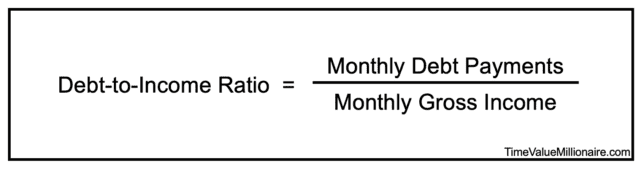

3. Debt-to-Income Ratio

Debt-to-income ratio is the percentage of our income allocated to paying off debt.

The formula for the debt-to-income ratio is:

The main application of this personal finance calculation is lenders using this ratio in determining loan eligibility as well as setting their associated rates.

A high debt-to-income ratio signals to a lender that an individual has other debt obligations relative to their income. Because the individual has less cash-on-hand every month (due to their income going towards paying other debts), they are therefore more at risk to potentially default on a new loan.

This would result in either denial of a new loan application or the loan being granted but with a higher interest rate in order to cover the lender’s risk.

On the other hand, a low debt-to-income ratio signals that an individual has little to no debt. From a lender’s perspective, this individual would be considered low risk and less likely to default on a new loan due to their income not being tied up in other forms of debt.

The end result is not only approval of a loan application but often with a much better interest rate.

4. Net Worth

Net worth subtracts the value of our financial liabilities from our financial assets in order to determine our financial worth.

The formula for net worth is:

The best way to think of our net worth is as a financial report card.

In other words, our net worth is the aggregated sum of our financial habits added up over time.

Financial habits that lower our net worth include:

- Buying things on credit

- Spending more than we make

- Investing in bitcoin (shots fired!) 🙂

On the other hand, financial habits that increase our net worth include:

- Consistently saving and investing

- Decreasing expenses

- Paying down debt

When calculating our net worth, below is a comprehensive list of what the Federal Reserve considers assets and liabilities:

| Assets | Liabilities |

|---|---|

| Transaction Accounts (Checking/Saving/Money Market Accounts) | Mortgages |

| Certificates of Deposits (CDs) | HELOCs |

| Savings Bonds | Other Residential Debt |

| Bonds | Credit Card Balances |

| Stocks | Line of Credit |

| Pooled Investment Funds | Line of Credit |

| Retirement Accounts | Educational Loans |

| Cash Value Life Insurance | Vehicle Loans |

| Business Equity | – |

| Vehicles | – |

| Primary Residence Equity | – |

| Other Residential Properties | – |

| Equity in Nonresidential Properties | – |

| Other Managed Assets | – |

We can easily track our net worth manually via Excel/Google Sheets or automatically with a tool like Personal Capital. I personally use both methods in order to double check my work.

Finally, there is another variation of net worth that we can calculate called liquid net worth.

Liquid net worth is defined as the total amount of cash available after deducting short-term liabilities from one’s liquid assets. This metric can be useful in determining how much cash we could generate on hand in a relatively quick turnaround.

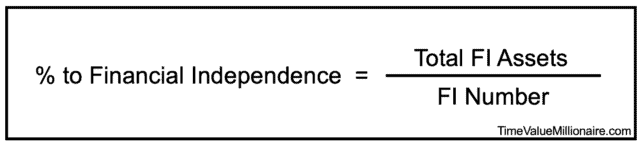

5. % to Financial Independence

% to Financial Independence (FI) measures how close we are to financial independence.

The formula for % to FI is:

One of the biggest misconceptions that I’ve seen online are people confusing this metric with net worth.

While they are similar, they measure completely different things.

As a reminder, net worth subtracts the value of our financial liabilities from our financial assets in order to determine our financial worth. On the other hand, % to FI only looks at our FI assets or the assets that we will rely on in financial independence relative to our FI Number.

The best example in illustrating the difference is one’s home. When calculating our net worth, we should absolutely include our primary residence. On the other hand, unless we plan on selling our home in retirement, it should not be counted as a FI asset.

For a more detailed guide on calculating our % to FI, feel free to check out my post: 5 Steps to Calculate Your Progress to Financial Independence. Furthermore, I have been documenting my % to FI journey over the last 8 years on my about page.

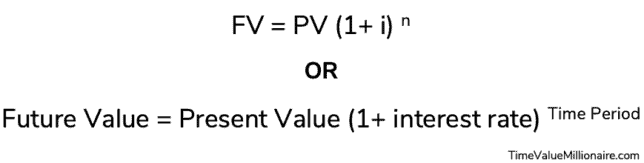

6. Time Value of Money

The time value of money is the king of the personal finance calculations.

It is the concept that money is more valuable today versus an identical sum in the future.

The formula for the time value of money is:

We can use the time value of money in order to answer any of the following questions:

- Future Value of Money (FV): What will my money be worth in the future?

- Present Value of Money (PV): What is my money worth today?

- Interest Rate (i): What interest is my money earning?

- Time Period (n): How long is my money being invested?

For a step-by-step guide on how to leverage this powerful calculation, I go into a lot more detail in my post “The Importance of the Time Value of Money.”

In that post, I go over some real world applications including

- Calculating loan payment & amortization schedules

- Calculating how much money is needed to retire

- Optimizing our lottery winnings 🙂

Final Thoughts

At the end of the day, personal finance doesn’t need to be a shot in the dark.

By understanding basic personal finance calculations, we can enable ourselves to make the best decisions for our specific financial situations.

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.