In the most recent Survey of Consumer Finances, the Federal Reserve revealed that the median U.S. household’s total net worth was $121,740.

However, this popular metric is not the only way to diagnose our financial health.

Instead, we can look to liquid net worth as another measure to assess the state of our personal finances.

In this article, we will be covering:

- What is Total Net Worth?

- What is Liquid Net Worth?

- How to Increase Your Liquid Net Worth

What is Total Net Worth?

We can define total net worth with the following formula:

Total Net Worth = Total Value of All Assets – Total Value of All Liabilities

Below is a comprehensive list of what the Federal Reserve considers assets and liabilities when calculating our total net worth:

| Assets | Liabilities |

|---|---|

| Transaction Accounts (Checking/Saving/Money Market Accounts) | Mortgages |

| Certificates of Deposits (CDs) | HELOCs |

| Savings Bonds | Other Residential Debt |

| Bonds | Credit Card Balances |

| Stocks | Vehicles |

| Pooled Investment Funds | Lines of Credit |

| Retirement Accounts | Educational Loans |

| Cash Value Life Insurance | Vehicle Loans |

| Other Managed Assets | Other Loans |

| Vehicles | – |

| Primary Residence Equity | – |

| Other Residential Properties | – |

| Equity in Nonresidential Properties | – |

| Business Equity | – |

| Other Managed Assets | – |

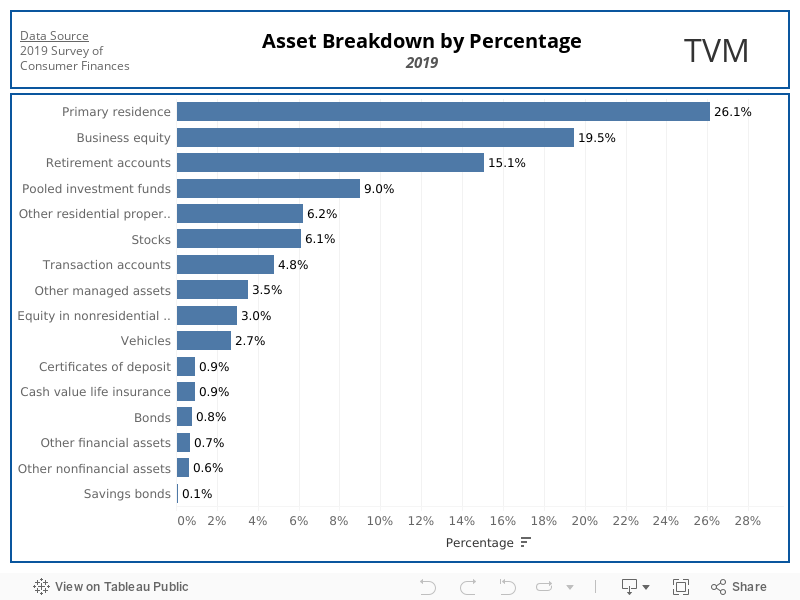

Total net worth is comprised of both liquid assets (i.e. stocks, bonds, transaction accounts) and non-liquid assets (i.e. primary residence equity, vehicles, business equity). In 2019, the median value of all these combined assets for U.S. household’s was $227,500.

And here is how that $227,500 break downs by percentage in each asset category:

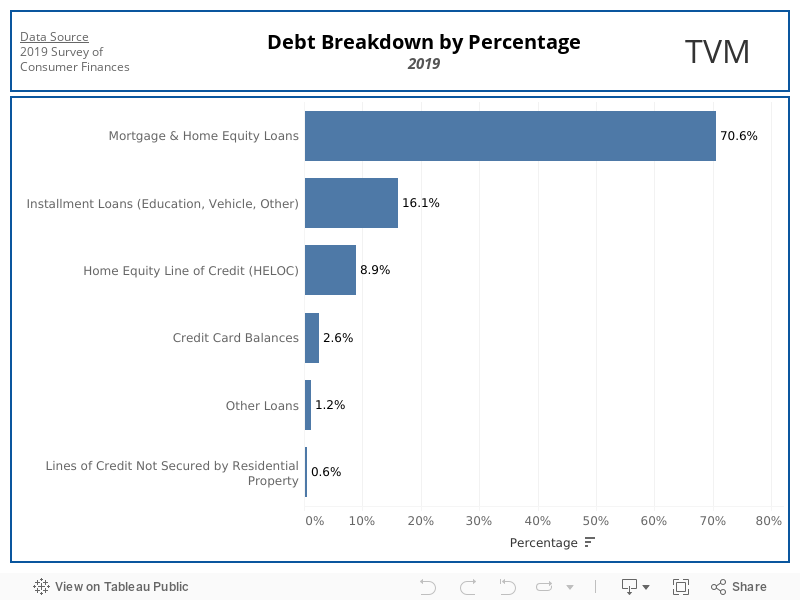

Total net worth is also comprised of both long term debt (i.e. mortgages) as well as short term debt (i.e. credit card balances). In 2019, the median value of all combined debt for U.S. household’s was $65,000.

Likewise, here is how that $65,000 breaks down by percentage in each debt category:

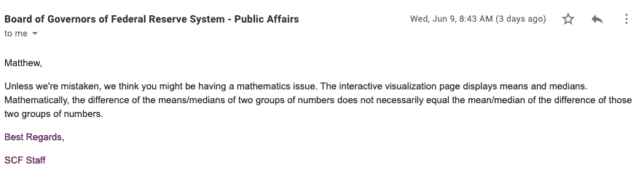

Quick Side Note: If you subtract these values, you will not get the $121,740 median net worth mentioned earlier in this article. This is because – as the Federal Reserve kindly reminded me – medians are not additive 🙂

What is Liquid Net Worth?

Liquid net worth can be defined as the total amount of cash available after deducting short term liabilities from one’s liquid assets.

As a result, the formula to calculate our liquid net worth is as follows:

Liquid Net Worth = Total Value of Liquid Assets – Total Value Short Term Liabilities

Liquid assets are assets that can be quickly and easily converted into cash.

This differs from non-liquid assets like property and retirement accounts, where there is significant friction (taxes, fees, etc.) preventing the asset from being readily converted into cash.

Furthermore, we are only using the total value of our short term liabilities because we are not expected to pay all of our loans at one time – this is similar logic in how businesses calculate net liquid assets.

This means that the only liabilities included are debt payments due in the near term (<30 days). If we are not considering assets like home equity, then it only makes sense to not include the entire loan against the home in our liquid net worth calculation.

With this mind, we can recreate the table from earlier to only include assets and liabilities that we should use in calculating our liquid net worth.

| Liquid Assets | Short Term Liabilities* |

| Transaction Accounts | Credit Card Balances |

| Certificates of Deposits | Vehicles Payments |

| Savings Bonds | Educational Loan Payments |

| Bonds | Personal Loan Payments |

| Stocks | Mortgage Payments |

| Pooled Investment Funds | HELOC Payments |

How to Increase Your Liquid Net Worth

As a reminder, the formula for Liquid Net Worth is:

Liquid Net Worth = Total Value of Liquid Assets – Total Value Short Term Liabilities

Therefore if we want to increase our liquid net worth, we need to either increase the value of our liquid assets or minimize our short term liabilities.

With that being said, let’s look at 4 different ways in order to increase our liquid net worth.

Adjusting Your Asset Allocation

The easiest way to increase our liquid net worth is adjusting what assets that our money is flowing into.

As an example, let’s assume that we currently invest $1,000 a month into an employer sponsored retirement plan. However, let’s assume we recently decided that our emergency fund needed some extra padding.

We can temporarily decrease our contributions into that retirement account and maneuver that cash instead into where we store our emergency fund.

Increasing Your Savings Rate

Another easy way to increase our liquid assets is by increasing our savings rate.

This allows us to take the additional funds that we save and invest them into more liquid assets.

This can be done with several different methods:

- Decreasing our Big 3 Expenses

- Decreasing Non-Essential Recurring Expenses

- Automate our Savings

Negotiating a Raise

We can also increase our liquid net worth by increasing our monthly cash flow.

This can be done by either switching jobs or doing what I did and internally negotiate a 25% raise.

Paying Down Short Term Debt

On the liability side of the equation, the single best option is paying down our short term debt.

In my 2021 Q1 Financial Update, I discussed how we decreased our investment contributions for months in order to pay down our car loans.

By paying our car loans off early, we reclaimed that monthly outflow of cash and increased our savings rate… acting like a double whammy with increasing our liquid net worth!

Final Thoughts

After crunching the numbers some more, I found something interesting.

When looking at U.S. household’s asset breakdown, only 22% of those assets are liquid while the other 78% are non-liquid. This general lack of liquidity can potentially create two problems:

- We can’t cover a financial emergency

- We can’t capitalize on financial opportunities

As a result, it’s important to understand what our liquid net worth is in order to ensure that not only are we maximizing our returns but that we also have enough cash on hand just in case.

Do you have a liquidity strategy? How does your liquid / non-liquid split compare to U.S. households?

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered to be advice, research or an invitation to buy or sell any securities, please see my Terms & Conditions page for a full disclaimer.