At some point, you may have heard of a concept called the latte factor.

In a nutshell, the latte factor is the idea that spending small amounts of money on a regular basis can add up over time. Furthermore, this money can instead be saved/invested over time in order to build wealth.

However, whether we are talking about lattes or avocado toast, the truth is that there are more effective ways in order to build wealth rather than cutting out these small expenses.

* Spoiler Alert: Lattes and avocado toast are not preventing people from buying homes *

Let’s dive in.

Trimming Bigger Expenses Yields Bigger Savings

I want to be clear that I am not denying the math behind the latte factor.

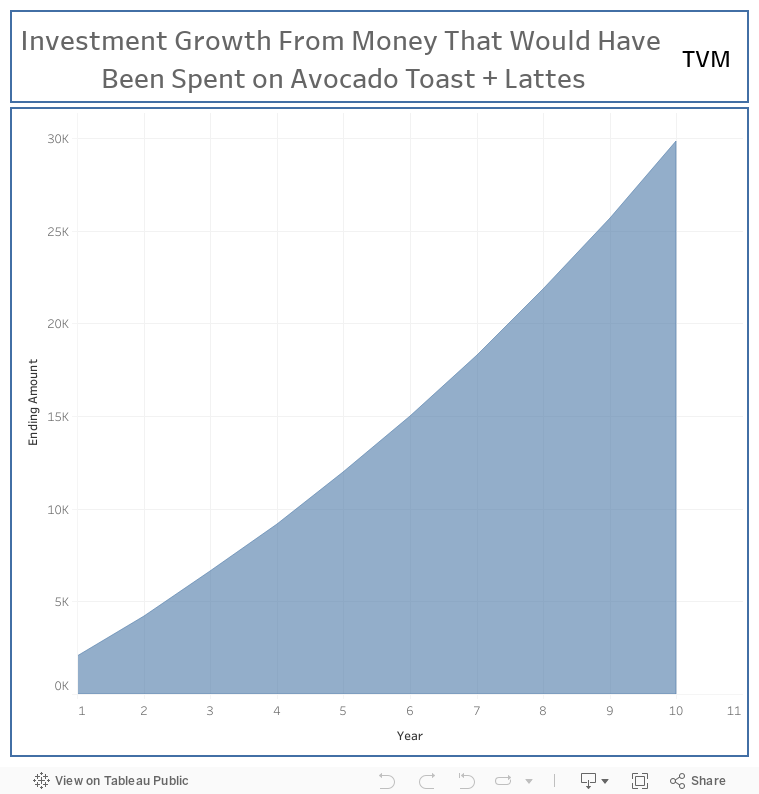

The truth is that small amounts of money do have the ability to significantly grow over time due to compound interest. To demonstrate the latte factor in effect, let’s model out a scenario under the following assumptions:

- Average Price of Avocado Toast: $6.78 (Source: Time)

- Average Price of Grande Latte at Starbucks: $3.65 (Source: Starbucks)

- Average Rate of Return of 50/50 Portfolio: 8.29% (Source: Vanguard)

- We enjoy a daily avocado toast & latte 15 days out of the month

Here is how the money not spent on lattes and avocado toast would compound over a time period of 10 years:

The above model demonstrates how cutting out lattes and avocado toast can translate into decent wealth. However, it’s pennies compared to what would happen if we focused on our much larger expenses.

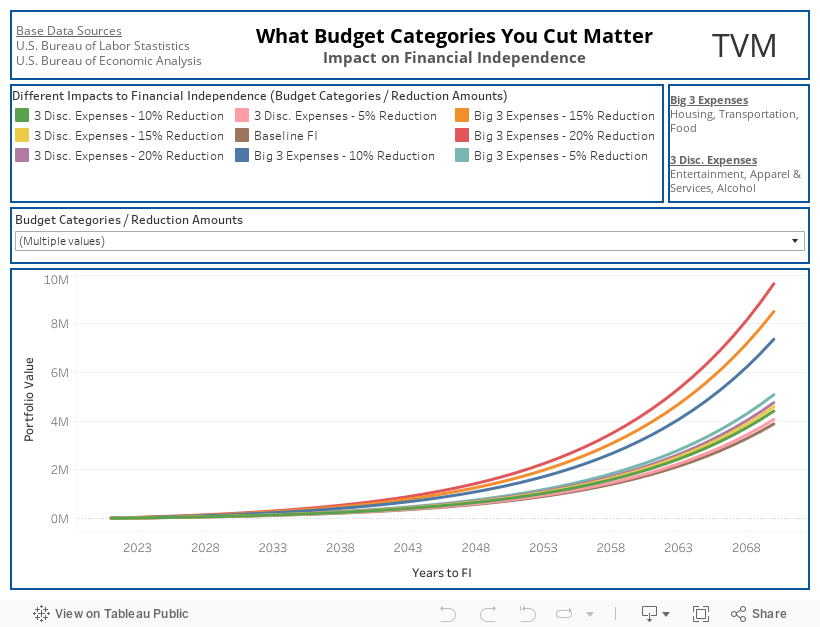

To demonstrate this, here is where our wealth would be if we instead focused on trimming down our big 3 expenses that make 64% of all our spending vs 3 smaller/discretionary expense categories:

If you are interested in my full analysis on how the big 3 expenses impact our path to financial independence, you can find my full case study here.

The truth is that we should not be penny wise and pound foolish. With that being said, we can and should trim down on smaller expenses that don’t meaningfully increase our happiness. On the other hand, if there are small and simple pleasures that genuinely make us happier, we shouldn’t feel guilty for not cutting them out. This will only lead to feelings of deprivation.

Instead, our focus should be on decreasing our big 3 expenses. Not only are we able to generate substantially more wealth via the savings generated from cuts to these expense categories, but it also enables ourselves to “overspend” in other areas of our lives that make us happier.

Finally, if we actively budget for these smaller expenses, what’s the big deal?

I personally love buying specialty coffee that can range from $30 – $80 a bag. This is apart of my budget and is not money that I look at and say “I should be investing this instead.” Despite buying expensive coffee, I was able to buy a home at age 25 and become 12.8% financially independent by age 27. This was all made possible by keeping my big 3 expenses in check.

Expenses Are Only One Part of the Wealth Equation

The reality is that we can only cut our expenses by so much.

And cuts to these smaller expenses will not make a difference in whether we can afford a home or become financially independent.

To demonstrate this, here is a fun thought experiment:

According to the Federal Reserve, the median home price in the U.S. is currently $454,900. A 20% down-payment on a house of this price would translate to $90,980 (ouch).

In other words, we would need to forgo approximately ~8723 lattes & avocado toast everyday for ~24 straight years to afford the median priced home in the U.S. today (not even a median priced home in 24 years). This can take even longer for those trying to afford a home in HCOL cities.

Instead of cutting out smaller expenses for 24 years, we could shift our focus to the other part of the equation: increasing our savings rate via actively increasing our W2 and passive income.

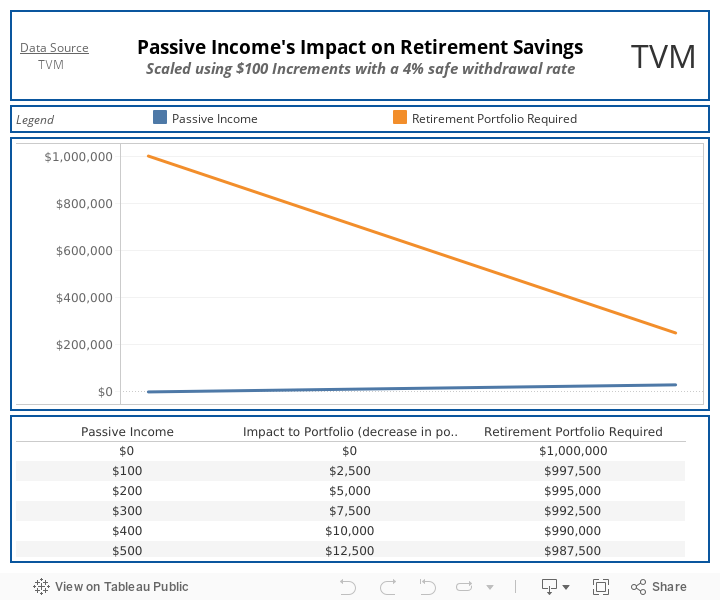

However, I want to put special emphasis on passive income. That is because passive income has the ability to significantly decrease the amount of money required for financial independence:

Final Thoughts

Whether we are trying to become financially independent or purchase a home, the truth is that blaming avocado toast and lattes makes a much better headline then:

- Stagnant Wages

- Rising Prices across the Board

- Housing Affordability

At the end of the day, our ability to achieve our financial goals depends on a mixture of things within (savings rate) and beyond (inflation) our control. However, giving up small pleasures in our lives is neither the optimal nor the only solution in order to build wealth.

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.