Location, Location, Location.

Where we choose to live is one of the most important financial decisions that we’ll ever make.

As a result, today’s post will be examining the impacts of living in a HCOL vs LCOL area.

More specifically, we will be looking at:

- HCOL vs LCOL – What’s the difference?

- HCOL vs LCOL Areas Across the United States

- The Pros & Cons of HCOL vs LCOL Areas

Let’s dive in.

HCOL vs LCOL: What’s the difference?

What is Cost of Living?

Cost of living refers to the amount of money needed in order to cover our expenses.

Our individual cost of living is influenced by a variety of factors including:

- Our Lifestyle Choices

- Our Family Size

- Our Age/Health

- Where We Live

In 2019, the average American household’s average cost of living was equivalent to $63,036.

The dominant expense that drives our cost of living is what we pay for housing, accounting for 33.2% of our expenses on average. For that reason, we will explore how living in a HCOL vs LCOL area can impact our personal finances.

The Definition of HCOL vs LCOL Area

HCOL stands for ‘high cost of living.’

As a result, a HCOL area refers to an area that is relatively more expensive to live in.

On the other hand, LCOL stands for ‘low cost of living.’

Furthermore, a LCOL area refers to an area that is relatively less expensive to live in.

HCOL vs LCOL Areas Across the United States

Using a cost of living index, we can identify HCOL vs LCOL areas across the United States.

When looking at the below data visualization, keep the following in mind:

- A cost of living index < 100 is a LCOL area (costs are lower then average)

- A cost of living index > 100 is a HCOL area (costs are higher then average)

To better understand what we are looking at, let’s look at an example.

The most expensive and least expensive states are Hawaii & Mississippi respectively.

Hawaii has a cost of living index of 193.3, meaning that living in Hawaii costs 93.3% more than the average cost to live in America. Likewise, Mississippi has a cost of living index of 83.3, meaning that living in Mississippi costs 16.7% less than the average cost to live in America AND 110% less than the cost to live in Hawaii.

Furthermore, a Mississippi family living on $50,000 / year would need to make at least $115,500 a year just to maintain the same lifestyle in Hawaii. Crazy.

However, there are also variations in the cost of living within each state.

Here are the cost of living indices for 6 metro areas in Missouri:

What is responsible for these variations?

When digging deeper into the data, we can begin to see price fluctuations for the following budget categories:

| Metro | Index | Housing | Grocery | Transportation |

| Joplin MO | 82.6 | 65.8 | 89.9 | 92.0 |

| St. Louis MO | 87.1 | 74.6 | 99.5 | 86.3 |

| MO (Average) | 89.8 | 80.3 | 95.0 | 92.4 |

| Springfield MO | 90.4 | 77.9 | 100.1 | 93.8 |

| Jefferson City MO | 90.7 | 77.8 | 93.9 | 103.1 |

| Kansas City MO | 93.7 | 98.1 | 89.5 | 86.2 |

| Columbia MO | 94.1 | 87.7 | 97.2 | 92.9 |

| USA | 100 | 100 | 100 | 100 |

We can see that Joplin, MO is 7.2% cheaper relative to the average cost of living in Missouri because housing is 14.5% less expensive! And as we saw in our case study on the big 3 expenses, this can have a major impact on our path to financial independence.

If you are curious on what cities are HCOL vs LCOL, an easy way to find out is by using Nerd Wallet’s Cost of Living Calculator.

HCOL vs LCOL: The Pros & Cons

The Pros of Living in a HCOL Area

HCOL Areas have more higher paying jobs

We have all heard the value of getting a college degree.

However, where we decide to work can significantly impact the ROI of that degree.

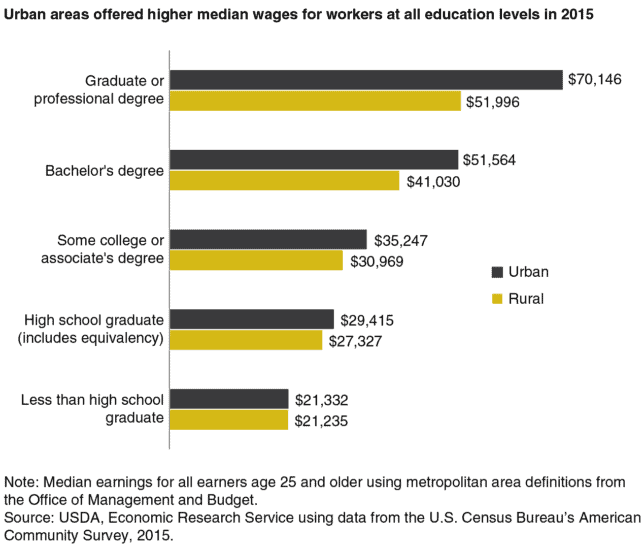

According to the U.S. Economic Research Service, urban areas (generally considered HCOL) consistently offer higher median wages for all workers at all levels of education compared to rural areas (generally considered LCOL).

Why is this? The U.S. Economic Research Service goes on to explain several differentiating factors between HCOL vs LCOL areas:

Businesses that provide skill-intensive employment may be clustered in urban areas, where a larger market allows for closer proximity to customers and suppliers, shared infrastructure, and better matching between employers and employees. The density of businesses and people in urban areas may also facilitate the promotion and adoption of innovative ideas. These benefits may enhance the productivity of businesses and workers, contributing to higher urban wages.

Source: US USDA Economic Research Service

So while living in a HCOL area does cost more, it can increase our chances of earning 6 figures.

HCOL Areas can speed up our path to financial independence

A popular strategy to speed up the path to financial independence is working in a HCOL area and then retiring to a LCOL area.

This strategy offers three awesome benefits:

First, earning a higher income in a HCOL area can enable us to build our investment portfolio a lot faster. This can result in reducing our runway to achieving financial independence.

Secondly, all else being equal, one’s financial independence number in a LCOL area will be smaller than one’s financial independence number required in a HCOL area. As we saw in the Missouri + Hawaii example from earlier, we can maintain the same lifestyle for less by moving to a LCOL area.

Finally, our investment portfolio will stretch farther in a LCOL area. A Lean FIRE lifestyle in a HCOL area can potentially translate to a Fat FIRE lifestyle in a LCOL area.

The great part about this strategy is that we don’t have to move from L.A. to the woods of Idaho to realize these benefits. As we saw earlier, there is a lot of variation in the cost of living even within the same state.

The Cons of Living in a HCOL Area

Life costs more in HCOL Areas

The most obvious disadvantage to living in a HCOL area is that life costs more.

This can create hardships if someone is not earning at least the living wage for that area.

However, to really thrive, one would need to earn more than the living wage.

If you are thinking about moving to a HCOL area, I recommend checking out MIT’s Living Wage Calculator. This calculator lists the living wage for every county in the United States.

Financial Independence can take longer to achieve (if staying in HCOL Area)

We previously touched on how to take advantage of premium earnings in a HCOL area and then moving to a LCOL area to speed up our journey to financial independence.

If we wanted to remain in a HCOL area, then it can take us longer to reach financial independence. We are paying a premium on our lifestyle that can be cheaper somewhere else.

However, this isn’t necessarily a bad thing.

If living in a HCOL area truly enriches our life, then we should live there. There’s more to life then trying to reach financial independence as fast as possible.

The Pros of Living in a LCOL Area

LCOL Areas can offer a slower pace of life & better mental health

Instead of working 80+ hours a week making the big bucks in a HCOL area, we can opt instead to slow things down to enjoy our lives and improve our health.

In a study published in the National Library of Medicine, working longer hours can result in increased risks of:

- Cardiovascular and cerebrovascular diseases

- Hypertension

- Diabetes

- Depression & Anxiety

- Work Stress

- Health Behaviors (smoking/alcohol intake, physical activity)

- Sleep & Fatigue

- Occupational Injury

Instead of living in a HCOL area with a high-paying & stressful job, we can choose to live in a LCOL area & become time millionaires to do more things that enrich our lives.

Implementing Geoabritrage with remote work

If we are able to work remotely, then we may be able to implement a life-hack called Geoabritrage.

In a nutshell, this means working at a company located in a HCOL area but living in LCOL area and pocketing the higher salary. This works because identical salaries stretch differently based on where we live.

As an example, let’s look at what a 6 figure salary gets you in California vs Florida:

When looking at the below table, keep in mind the following assumptions:

- This assumes that someone is filing their taxes as an individual

- This does not include any local or county taxes

- This does not account for any income deductions (i.e. retirement accounts, health insurance, etc.)

- This assumes you are not exempt from FICA or Medicare

| STATE | GROSS SALARY | POST TAX SALARY | MONTHLY PAY | BIWEEKLY PAY | HOURLY PAY |

| CA | $100,000.00 | $67,476.24 | $5,190.48 | $2,595.24 | $32.44 |

| FL | $100,000.00 | $75,277.02 | $5,790.54 | $2,895.27 | $36.19 |

In the example above, working remotely in FL has the ability to increase one’s post tax salary by $7800!

This isn’t chump change either.

Using the time value of money, investing $7800 over a 30 time period making 10% on average would result in $1,283,053.38.

Not bad for doing the same work but instead living in a LCOL area!

The Cons of Living in a LCOL Area

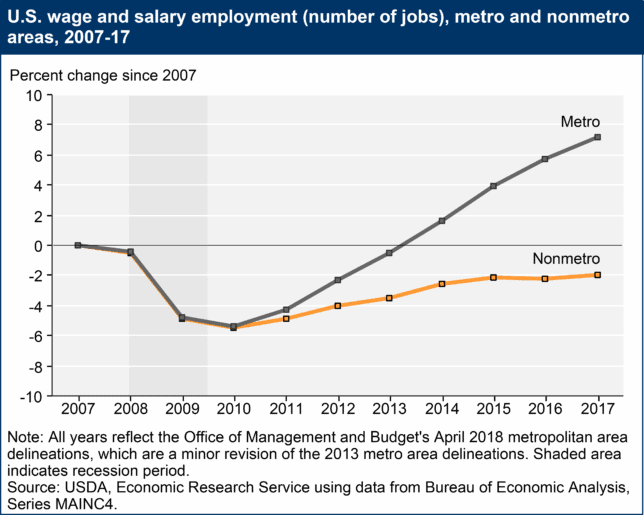

LCOL Areas can have a less stable job market

When it comes to the number of jobs available, there are more opportunities in HCOL vs LCOL areas:

Therefore, even minor disruptions in the economy can have a large impact on employment opportunities in LCOL areas due to less jobs available.

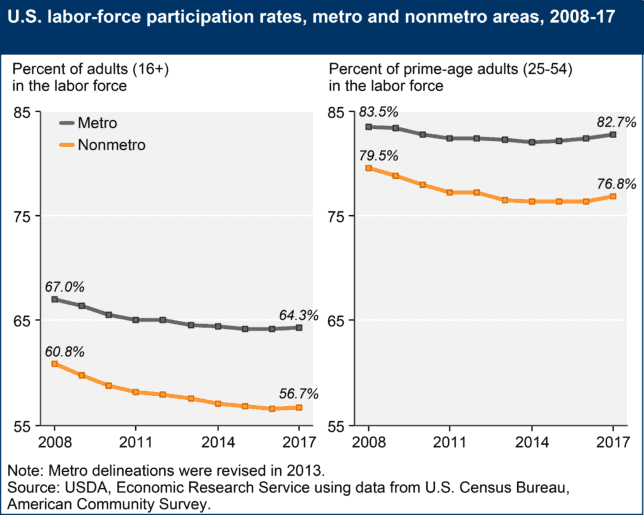

This is not as big of an issue for HCOL areas that have consistently higher rates of labor force participation:

Financial Independence can take longer to achieve in a LCOL

Generally speaking, there are less high-paying jobs in LCOL areas relative to HCOL areas.

This lack of wage growth, along with the fact that we can only cut our expenses so much, makes it harder to increase our savings rate

The result is a potentially longer road to financially independence.

And if you are apart of the antiwork movement and hate the idea of working then this can represent a major disadvantage to living in a LCOL area.

Final Thoughts

When it comes to living in HCOL vs LCOL areas, there is a lot to consider.

From a financial perspective, the decision to live in a HCOL vs LCOL area can have a dramatic impact on what our path to financial independence looks like.

From a life perspective, we should consider our physical/mental health as well as what will maximize our pursuit of happiness.

As part of your financial planning, have you ever considered living in a HCOL vs LCOL area? If so, what were the deciding factors?

Thank you for reading 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.