Welcome to the third TVM Financial Update of 2022.

The purpose of these quarterly financial updates is to crunch the numbers, visualize the data and share our progress towards becoming financially independent.

For a recap of what happened so far in 2022, you can find my Q1 + Q2 updates here:

Life Update

Summer is over and Fall is officially here!

Except not really because well… Florida 😛

While it has been a busy and fun Summer, I’m happy to start winding down into Fall.

With that being said, here are some highlights from the last 3 months:

I attended my first FinCon! This wasn’t on the radar until I saw that it was in Orlando, Florida this year (close to home). And to be honest, I had a blast. If you want to read more about my experience, I recently posted my 3 biggest takeaways from FinCon 22.

We went on our first vacation since having our baby. We went to Tampa, Florida for a getaway weekend to see Jack Johnson & Ziggy Marley. It was much needed time off to relax and recharge our parental batteries for another couple months!

I’ve been working on another passion project. To quote Hamilton (my favorite film/album ever):

Why do you write like you’re running out of time?

Hamilton

Write day and night like you’re running out of time?

Every day you fight, like you’re running out of time

Keep on fighting, in the meantime-

(Non-stop!)

In all seriousness, I’ve been writing articles “non-stop” for a new website that I’ll be launching this Fall. But that’s all I will say on that for now 🙂

“OK Man… How did you do financially this quarter? Show me the money!”

You got it.

Financial Update

A quick note: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.

Let’s dive in.

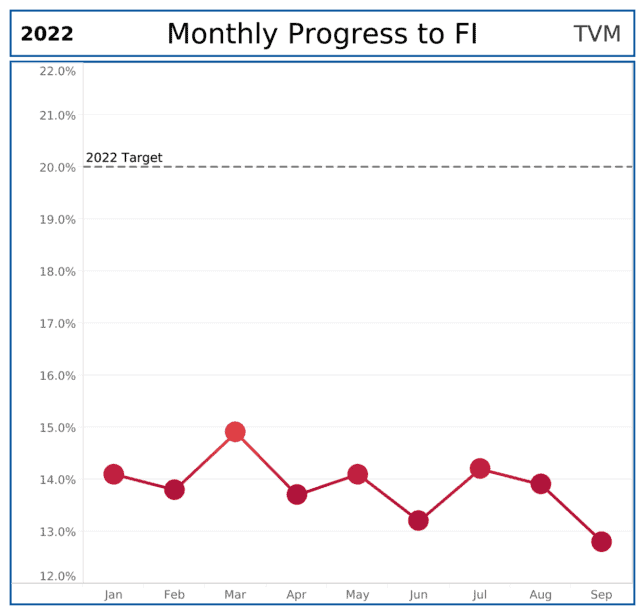

Progress to Financial Independence

From Q2 2022 to Q3 2022, our % FI decreased 0.4% from 13.2% to 12.8%.

As a reminder, our % FI is a function of two variables:

- Our average monthly spending

- The total balance of our FI Assets

To be honest, between some major spending (both planned and unplanned) & the markets going through a fritz, I was shocked to see the percentage decrease was as small as it was.

Between one last major home project that we have planned this year & current market conditions, I am not confident that we will hit our 20% FI Goal for 2022.

However, we are not upset about this.

Our portfolio is at point where compound interest + market volatility have a greater impact than just pure savings each month. It’s both a blessing and a curse!

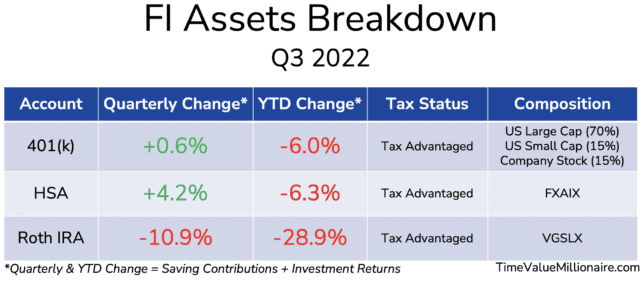

Asset Breakdown

The above table is a breakdown of our current FI Assets.

Do my eyes deceive me? Is that green that I see?

While we are still overall mega red for the year, it was nice to see that the 401(k) and HSA are now back to ONLY “single digit” loses for the year. *knock on wood*

The 401(k) was positive because of my company stock performing well. This single stock that I own has been acting as a hedge against all the other market indices for the last two quarters.

The HSA was positive because of additional contributions that my employer made due to Mrs. TVM & I completing our annual physicals. Free money.

The Roth IRA is being killed due to the rising interest rate environment (VGSLX is a REIT fund).

Because we own our house, I’ve been recently thinking about re-balancing our Roth IRA in order to readjust our overall real estate exposure. If we make any adjustments, I’ll note it in a future financial update.

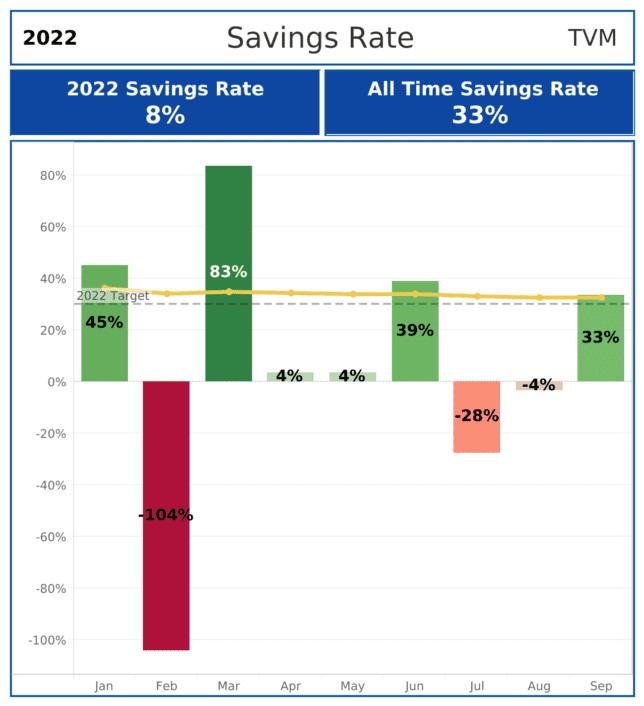

Savings Rate

Our 2022 savings rate is currently at 8%, down 4% from Q2 2022.

This is our second quarter as a single income household.

As a result, when unplanned expenses do pop up, they have a much larger impact on our savings rate (I’m looking at you July).

While our savings rate is currently positive, I don’t think we will end the year positive.

We have one last major renovation slated for the house that costs as much as a brand new car. Because we are paying cash for said renovation, we will probably set a record for the lowest savings rate ever.

Furthermore, we also took out a loan for a brand new AC system that died back in September (in Florida, in Summer).

As a result, we are probably going to lower our retirement savings for a few months to get that system paid off due the loan’s interest rate being ~15%. While we can technically pay the system off immediately – we don’t want to completely drain our emergency fund.

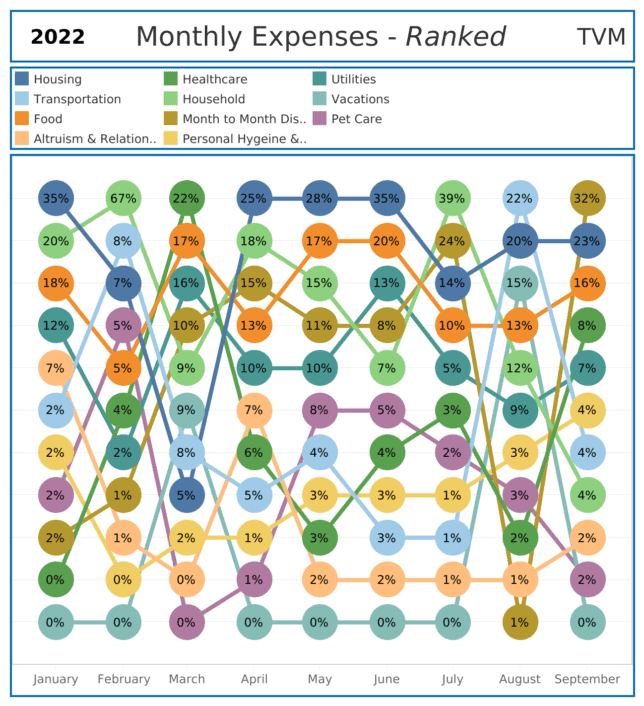

Monthly Expenses

Let’s take a look at our Expense Sankey, aka Mrs. TVM’s favorite data visualization.

The above graphic visualizes how our monthly expenses rank month over month. The percentages in the individual bubbles represent our % spending for each category for that month.

Here are some of the major spending highlights from this quarter:

- July

- Household: After 6 months of not having a dishwasher, we finally cracked. We have a small kitchen so dishes tend to pile up rather quickly; this has been an incredible space and time saver. Furthermore, we also replaced the couches I’ve had for 10+ years with couches that make a lot more sense for our house.

- Month to Month Discretional: I finally retired my Macbook of 10+ years. I was getting tired carrying a 100 ft Ethernet cable around the house (only way to connect to the internet). The computer was also incredibly slow, despite being a “hackintosh” with a 2 TB SSD & 64 GB of ram. After some encouragement from Mrs. TVM (who was also tired of tripping over my cable) I upgraded to a 2022 Macbook Air.

- August

- Transportation: Our 6 month car insurance premium was due

- Household: Another emergency repair of our 12 year old AC system… this was the point when we decided that we needed a new system.

- Vacation: Vacation in Tampa!

- September

- Heathcare: We both got some medical tests as a result of our annual physicals.

- Month to Month Discretional: Mrs. TVM & I both had 5+ year old phones that could barely hold a charge anymore (despite replacing the batteries). So we splurged and both got new phones.

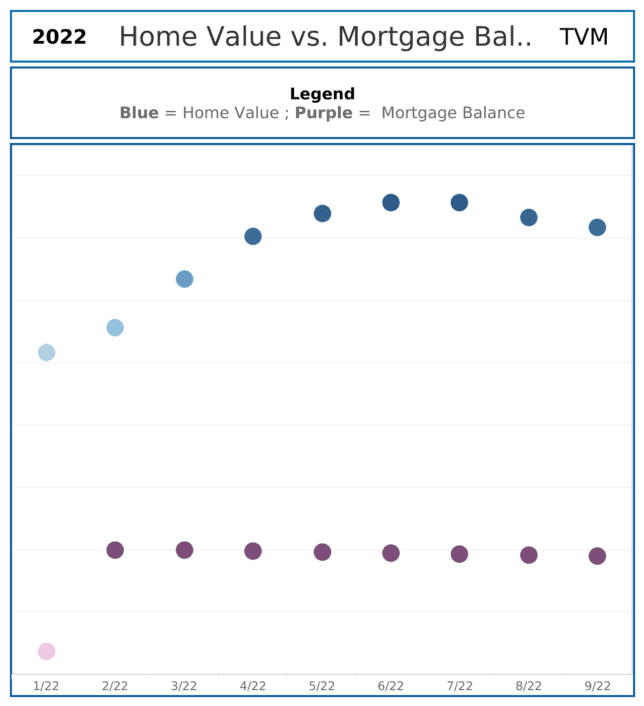

Home Value vs. Mortgage Balance

From Q1 2022 to Q2 2022, our home value decreased 2.4%.

I am very thankful that we executed our cash out refinance when we did.

At the time, our rate went from 3.5% to 3.625%. Furthermore, we were able to pull enough money out in order to cover a much-needed home renovation.

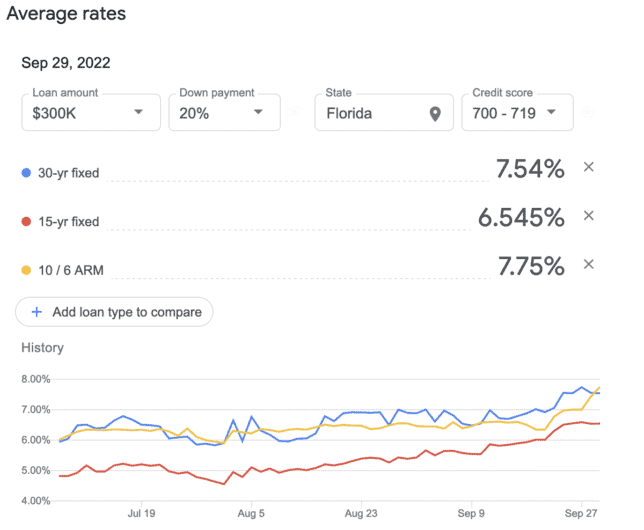

Here are mortgage rates as of a few days ago:

We don’t care how much equity that we have in our home, there’s no way we are going to do another cash out refinance to a rate ~ 5% higher. At this point, we will be funding future renovations the old fashioned way… pure savings baby!

Final Thoughts

From a life perspective, I’m looking forward to things slowing down, spending our first Autumn with our baby & enjoying a few PSLs.

From a financial perspective, I am excited to knock out a couple more big ticket items so that our 2023 can go back “to normal.” Whatever that means 🙂

Thank you for reading 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.