Welcome to the second TVM Financial Update of 2022.

The purpose of these quarterly financial updates is to crunch the numbers, visualize the data and share our progress towards becoming financially independent.

For a recap of what happened so far in 2022, you can find my Q1 update here:

Life Update

As I announced in our Q1 2022 Financial Update, Mrs. TVM & I are now officially parents.

And to be honest, the transition into parenthood has been the theme for the last three months.

It truly blows my mind how fast babies grow up. One day, you are carrying them around for hours with no issues and the next day holding them becomes a full-blown workout.

There are no honestly no words to describe the feeling of watching your child growing up and seeing their personality start to develop. Speaking of personality, our baby will only fall asleep / calm down to literally one song that I randomly found on Spotify.

I present to you the song that we have probably played 10,000 times (I’m not even exaggerating), Clap Your Hands by Kungs:

Disney music?

No.

Wheels on the bus?

No.

Clap Your Hands by Kungs?

TURN IT UP

– Our Child

I shit you not, if this song is not playing at all times… she is not happy.

Valentin Brunel (Kungs) – If you somehow come across this random blog on the internet, my household is likely responsible for 99% of the revenue that you’ve earned from this song. Also – thank you for all the nights where you have helped our child fall asleep 🙂

Financial Update

A quick note: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.

Let’s see how Q2 2022 shaped up!

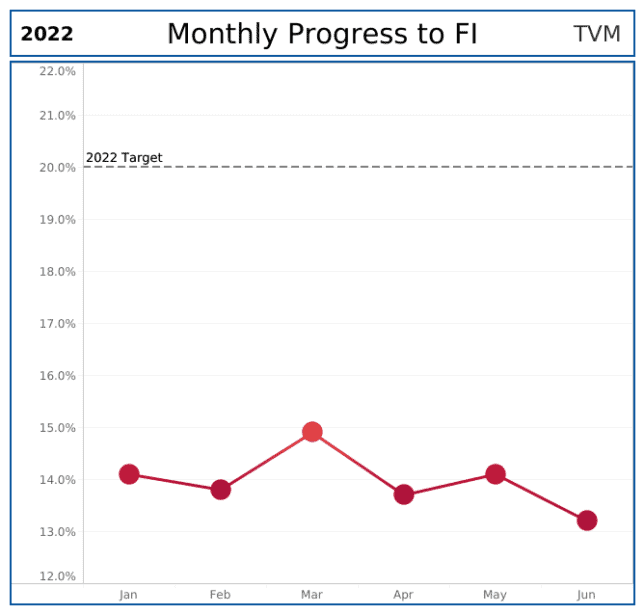

Progress to Financial Independence

From Q1 2022 to Q2 2022, our % FI decreased 1.7% from 14.9% to 13.2%.

As a reminder, our % FI is a function of two variables:

- Our average monthly spending

- The total balance of our FI Assets.

We didn’t have any crazy spending outliers this quarter. As a result, our decrease in % FI can be directly attributed to what’s been happening in the economy (factors beyond our control).

Our original goal was to be 20% FI by the end of 2022. However, with market volatility having a greater impact on our portfolio value than our savings rate, that goal is starting to look less likely.

At the end of the day, it is what it is.

If for some reason we don’t hit our goal, at a minimum it is nice knowing that we are lowering our average investment cost via an automated dollar cost averaging investing strategy.

Keep Calm & Save On.

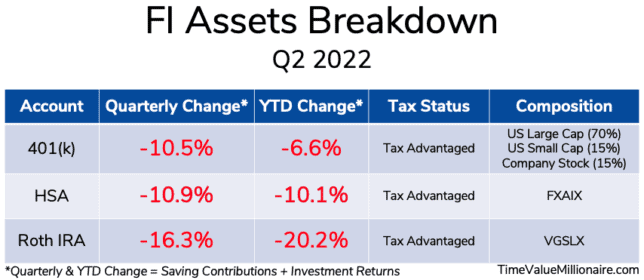

Asset Breakdown

The above table is a breakdown of our current FI Assets.

And from this table, we can see why our % FI number decreased as much as it did this quarter. That’s a whole lot of red!

When I was analyzing my 401(k) investment mix, I found something interesting.

I discovered that my companies stock was performing well and is acting as a sort of hedge against the negative performance from the other funds.

While I don’t believe in holding a ton of individual stocks (this is the only individual stock I own), I was pleasantly surprised to learn that this one stock was preventing my 401(k) from entering negative double digit territory for the year!

With that being said, I’m curious on how the global/national economy will be playing out over the course of the rest of the year. I’ll be closely watching what the Fed Reserve does to tackle inflation and might consider investing into some inflationary hedges like I Bonds.

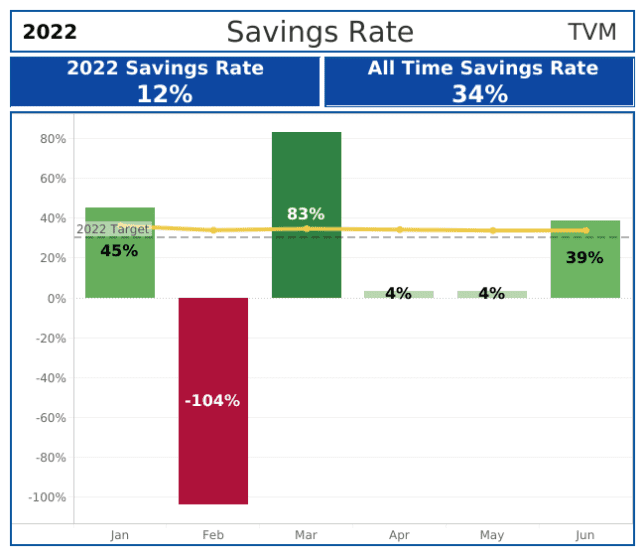

Savings Rate

Our 2022 savings rate is currently at 12%, up 4% from Q1 2022.

This is the first quarter where we are reporting our savings rate as a single income household.

So to be honest, I was just happy to see 3 months of positive savings rates!

I’m most proud of April. That’s because we were still in the green despite only receiving one paycheck. This was the case because I went unpaid in order to spend more time with our newborn.

Furthermore, we were stoked to see that we hit a savings rate closer to our long-term savings average in June. Although, we do anticipate July being an absolute blood bath from a savings perspective.

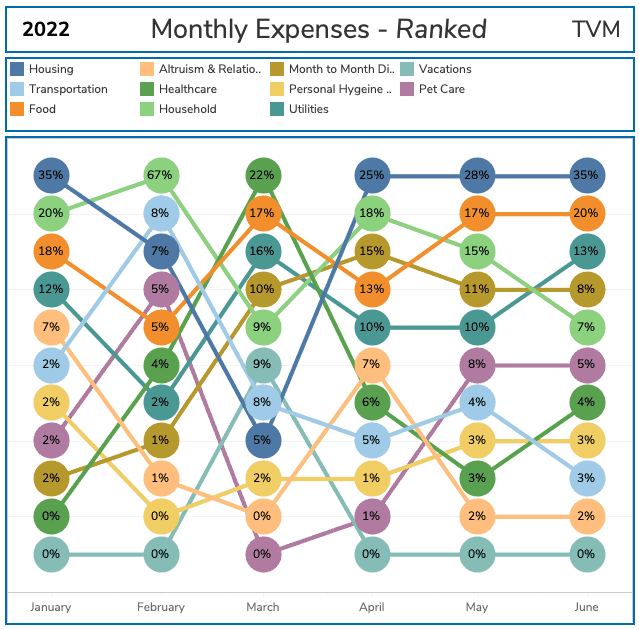

Monthly Expenses

Let’s take a look at our Expense Sankey, aka Mrs. TVM’s favorite data visualization.

The above graphic visualizes how our monthly expenses rank month over month. The percentages in the individual bubbles represent our % spending for each category for that month.

Here are some of the major spending highlights from this quarter:

- April

- Housing: When “Housing” becomes our top expense category, that’s how you know our spending is getting back to “normal” 🙂 The reason for the jump back to number 1 is that our first new mortgage payment was due since executing our cash-out refinance.

- Month to Month Discretional: Spending jumped due to an unexpected tax bill. This is the first year that I have ever had a tax bill in my life! Hopefully with downsizing to a single income family, along with our cute little tax deduction, we can go back to refund status! I also bought a lot of material to teach myself how to graft fruit trees (grafting knife/tape, the actual trees/scions, etc.)

- Household: We put a down payment on some new couches. It was fun doing “goldilocks testing” on the different couches like “This is too hard, this is too soft… this is just right!” Although it wasn’t as fun swiping the credit card 😛

- Altruism: Wedding presents, housewarming presents… etc.

- May

- Pet Care: The TVM pup got an ear infection and was also due for some annual vaccines. This coincided with a month where I needed to buy him more food.

- Month to Month Discretional: I found out that FinCon 22 is in Orlando this year! Because this happens to be in my backyard, I booked tickets to attend. I’m looking forward to learning as much as possible 🙂

- Household: We had our yearly AC tuneup and also bought an infant swing (totally worth it).

- June

- Honestly – nothing too juicy here. Spending was pretty vanilla.

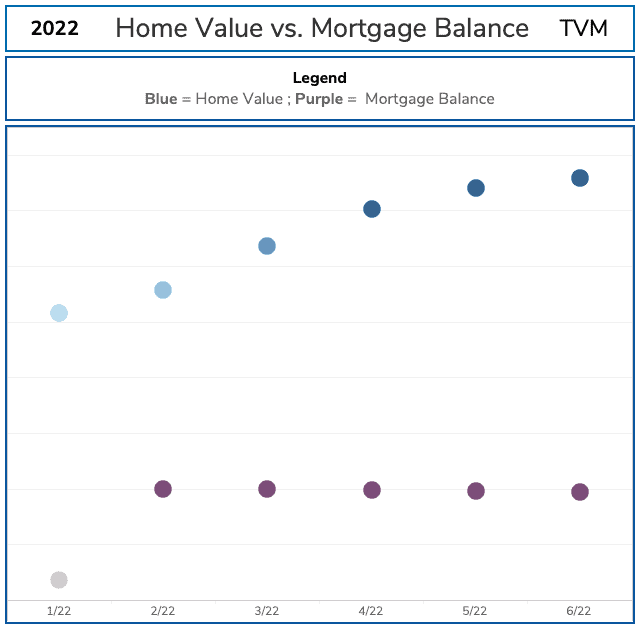

Home Value vs. Mortgage Balance

From Q1 2022 to Q2 2022, our home value increased 7.9%.

While our home is located in a well-established and desirable area, the % appreciation sometimes seems too good to be true.

As a result, depending on the interest rate environment, we may “realize” some of those gains by executing another cash-out refinance. If a bank is willing to write us a check, we might as well take advantage of that.

Another reason we are considering a cash-out refinance is that this house has the potential to be our forever home. We would use that money to do some big-ticket projects, like adding an additional bedroom, just in case our family were to get bigger in the future 🙂

Final Thoughts

Another quarter down on our path to financial independence.

While it wasn’t the best quarter we’ve had, we aren’t too worried about it.

That’s because we are too busy clapping our hands, moving our feet, two steps back, to the beat! 😛

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.