Over the years, we have heard tons of money advice.

Some based on facts, others not so much.

As a result, today we’ll be looking at 5 pieces of money advice that we hear all the time but should ignore.

Let’s dive in.

1. Carrying a credit card balance to build credit

The first piece of money advice you can ignore is carrying a credit card balance to build credit.

According to the Consumer Financial Protection Bureau, “paying off your credit cards in full every month is the best way to improve a credit score or maintain a good one [versus] carrying a [credit card] balance.”

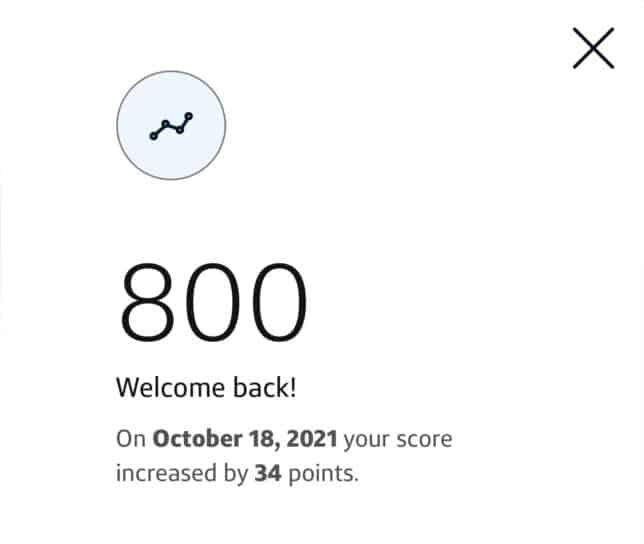

I have personally never carried a credit card balance. With that being said, when I checked my credit score a few months ago, this was what I got:

The reality is that carrying a credit card balance results in one thing: paying unnecessary interest to credit card companies.

According to the Federal Reserve’s Q3 2021 data, the average annual percentage rate for all credit cards was 14.54%. That is equivalent to paying $0.15 in interest for every $1.00 carried on a credit card.

And while that may not appear like a big deal, if left unchecked, that interest can compound.

As an example, imagine having a $1,000 credit card balance and making the $14.54 minimum interest payment every month.

This would take 12.3 years to pay off! Furthermore, $1153 would be going to interest payments alone!

More than the original balance!

So what can we do to actually improve our credit score?

According to FICO, we should focus on the following to build our credit:

As we can see, the amount we owe and our payment history make up 65% of our credit score.

With those two factors being the biggest influence on our credit scores, we should focus on doing things that can improve these portions. This includes but is not limited to:

- Paying our bills on time

- Maintaining a low credit utilization ratio (under 30%)

There’s no need to avoid credit cards.

Instead, we can leverage credit cards as a way to get rewards like cash-back or travel points in order to travel hack our way to financial independence.

2. Declining a raise to pay less taxes

The second piece of money advice you can ignore is declining a raise to pay less in taxes.

That is because the United States operates under a progressive tax system.

In a progressive tax system, you have a marginal tax rate and effective tax rate.

- The marginal tax rate is the tax rate applied to specific income brackets

- The effective tax rate is the total amount of taxes that an individual pays

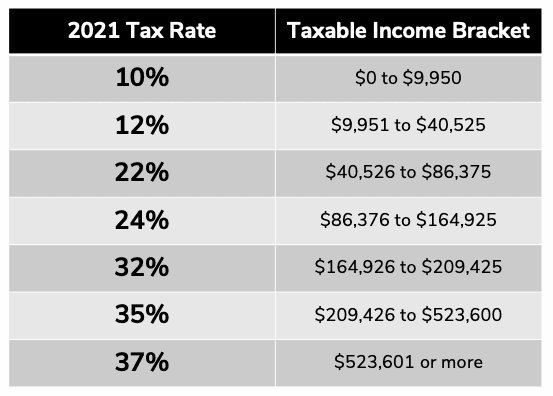

Let’s take a look at an example using the IRS’s 2021 Tax Rates:

*For simplicity, we are only looking at the federal tax rate*

Let’s assume that someone makes $40,000 a year. However, they deny a $1,000 raise because they claim that their effective tax rate would jump from 12% to 22%. This is not true.

At $40,000 a year, their effective rate would be equal to 11.5%.

Here’s the math:

- The first $9,950 is taxed marginally at 10%, resulting in $995 in taxes

- The next $30,050 is taxed marginally at 12%, resulting in $3,606 in taxes

- The total taxes on a $40,000 salary would be $4,601 or 11.5%

At $41,000 a year, their effective tax rate would be equal to 11.6%.

Here’s the math:

- The first $9,950 is taxed marginally at 10%, resulting in $995 in taxes

- The next $30,050 is taxed marginally at 12%, resulting in $3,606 in taxes

- The remaining $476 is taxed marginally at 22%, resulting in $104.72 in taxes

- The total taxes on a $41,000 salary would be $4,768.60 or 11.6% (not 22%!)

The fact is that a pay raise will always increase our overall net income. That is why I decided to internally negotiate a 25% raise.

If you are curious how taxes affect specific salaries state-by-state, I analyzed take-home pay for 6 figure salaries and $60,000 salaries for every state. The results were pretty interesting.

3. The stock market is too risky to invest in

The third piece of money advice you can ignore is that the stock market is too risky to invest in.

The fact is there is always risk associated with any type of investment that we make.

However, there are things we can do in order to minimize the risk associated with investing in the stock market. One of the most efficient ways to do so is investing in index funds as opposed to individual stocks.

An index fund is an investment fund designed to match the returns of a particular market index.

As an example, an S&P 500 index fund is designed to replicate the collective returns of the top 500 companies in the United States.

Index funds offer several major advantages:

- Market Diversification

- Lower Fees on Average

- Passively Managed

Using our example from earlier, let’s take a look at the average annual returns for the S&P 500:

Historically speaking, an S&P 500 index fund would have produced an average annual return of 7.8%.

The key with investing in the stock market is understanding that it’s a long-term game.

Furthermore, we need to be in control our emotions. By being aware of behavioral finance concepts that can impact our decision making, we can make more rational financial decisions.

4. Going to college is the only way to be successful

The fourth piece of money advice you can ignore is that going to college is the only way to be successful.

While a college degree can boost potential earnings, the truth is that there are plenty of jobs that pay 6 figures that don’t require a college degree.

In my case, all my degree ended up doing was checking a box. The only time I actually use it is when I write for this website 🙂

Instead of going to college and racking up student loans, one can instead use that time learning specialized skills that are in demand.

That is what I ended up doing this year.

I ignored company management telling me to get a masters degree and instead taught myself SQL (database language) and Tableau (data visualization software).

That helped me go on to successfully negotiate a 25% raise.

At the end of the day, success is not defined by whether or not you have a piece of paper.

Instead, it’s about the value that you can provide and proving it.

5. Investing takes a lot of money

The final piece of money advice you can ignore is that investing takes a lot of money.

The reality is that investing as a little as $100 / month can result in substantial returns.

This is possible due to the concept of compound interest.

The idea is that given enough time in the market, the money we invest begins to earn interest. That interest will then begin earning even more interest and so on.

To understand how powerful compound interest is, let’s look at an example.

Using the time value of money formula, we can calculate what investing $100 / month looks like over a period of 50 years:

At the end of a 50 year period, we would have $521,983 in savings.

However, only $60,000 (11.5%) of that $521,983 was from saving $100 / month.

The other $461,983 (88.5%) can be attributed to the interest that our money earned.

With that being said, don’t get discouraged and not invest because you don’t feel like you have enough money. The reality is that even investing small amounts can help you start your path to financial independence.

Final Thoughts

Money revolves around every aspect of our lives.

So naturally there is going to be a ton of money advice floating around, good and bad.

However, we should always make sure to do our own research.

What works for someone else may not work for you.

What is the worst financial advice that you’ve ever received?

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.