Welcome to the TVM 2022 Annual Report.

At the end of each year, I like to write an “Annual Report” in order to reflect on how my life and journey to financial independence have progressed.

What’s crazy to me is that this is my 3rd Annual Report since launching Time Value Millionaire. Time really does fly by.

If you are interested in my previous Annual Reports, you can find them here:

Without further ado, let’s dive in!

Life Highlights

The overall theme for 2022 can be perfectly summed up in the popular quote by Ralph Waldo Emerson:

Its not about the destination, it’s about the journey

Ralph Waldo Emerson

That is because the focus for 2022 has been living more presently. This represented a major shift from previous years’ mindsets where I was always daydreaming about financial independence and the future.

In the last 365 days…

Mrs. TVM & I are officially *real* parents. I say *real* because we’ve technically been fur parents to our golden retriever for the last two years 🙂 Jokes aside, we were incredibly blessed to have a healthy and unique child. From only falling asleep to a random EDM song that I found on the internet to chasing after the golden retriever in their walker like a maniac… it’s more than we could have ever asked for 🙂

We started living our lives again. We had a much needed R&R weekend in Tampa, where we got to see Jack Johnson & Ziggy Marley in concert. And while that was great, it was topped by getting to see HAMILTON in the theater for the first time 🙂 Because I am the biggest Hamilton fan on the planet, I splurged and got us very expensive orchestra seats. It was worth every penny 🙂

We completed a lot of major house projects. Get a home they say, it will be fun they say. We spent an ungodly amount of money on our house this year. The good news is that *knock on wood* a lot of these big projects were one-offs and won’t be recurring expenses. Some of the major projects that we knocked out included:

- Brand new air conditioner system (AC broke down in the FL summer)

- Brand new attic insulation (6+ feet of insulation blown into the attic)

- Brand new hurricane windows (replaced inefficient single pane windows that heated the house and contributed to the AC breaking down)

- Brand new siding (old siding was a cheap material from 80’s that wasn’t protecting the house from elements; we also installed new OSB and plywood as well)

- Brand new seamless gutters (didn’t have gutters on a large portion of house; the gutters that were on the house leaked all the time)

- Brand new appliances (ancient dishwasher & microwave broke down beyond repair)

- Brand new couches (replaced 20+ year old couches we had)

- Built attic flooring for extra storage (we have a small home)

I was accepted into the University of Florida Master Gardener (UFMG) Program. This is one of the biggest things that I am excited for in 2023. The program will give me a more well-rounded horticultural knowledge that I will be able to use in both our personal orchard as well as in our community.

I’ve been writing like I’m running out of time. If you knew this was a Hamilton quote, please comment on this article 🙂 From a TVM Perspective, I’ve been hunkering down on publishing articles for both TVM and several other websites. I also started another a website called TropicalTreeGuide.com where I’ve been writing about the other topic that I’m passionate about… warning: it’s mango mania over there right now 🙂

Financial Update

A quick note: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.

Let’s dive in.

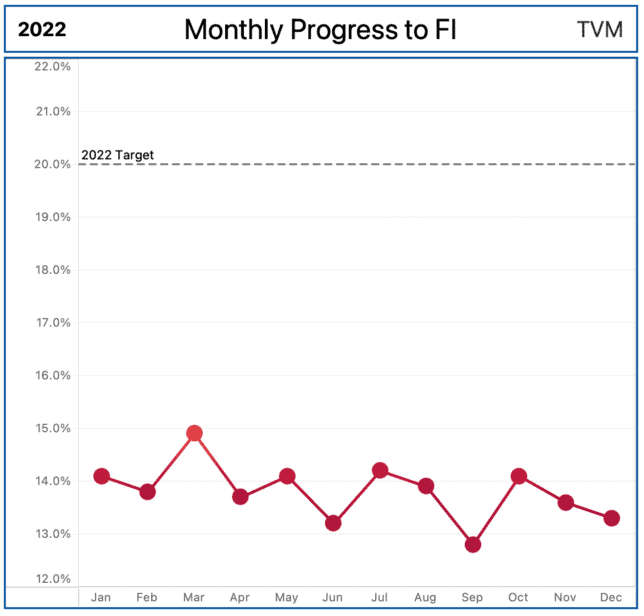

Progress to Financial Independence

From Q3 2022 to Q4 2022, our % FI increased 0.5% from 12.8% to 13.3%.

However, by the end of 2022, our % FI decreased 1.7% from 15% FI to 13.3% FI.

As a reminder, our % FI is a function of two variables:

- Our average monthly spending

- The total balance of our FI Assets

Considering 2022’s overall weak stock market performance and our record-breaking spending, I’m honestly going to consider this a win. Even though we came nowhere near the 20% FI goal, I truly was shocked that our % FI only decreased by 1.7%.

While we can’t control how our assets will perform next year, we are 100% in control of our spending.

That is why our primary focus for 2023 is getting back on track with a sustainable monthly budget. This shouldn’t be too hard because we are not planning to do any major house projects next year.

With that being said, we will not be setting a “% FI goal” for 2023. Instead, our goals will be centered around around metrics 100% within our control such as our savings rate.

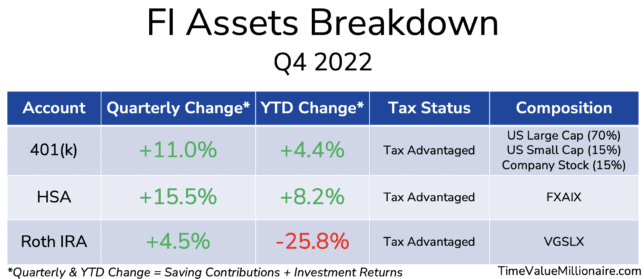

Asset Breakdown

The above table is a breakdown of our current FI Assets.

Much to my surprise, 2/3 of the accounts ended up in the green at the end of 2022.

Here is what I found when diving into the numbers:

The HSA was only positive due to consistent contributions to the account (aka no positive returns)

Likewise, the 401(k) was also only positive due to consistent contributions as well as the shocking over-performance of my company stock (only individual stock I own). With that being said, the total returns for both the US Large/Small Cap Funds were both negative.

The Roth IRA is still being killed by the rising interest rate environment. This is because the entire balance is invested in a single REIT Fund (which tends to be interest rate sensitive). As I mentioned in the Q3 2022 Financial Update, this may be re-balanced in the future due to us already having real estate exposure via our home.

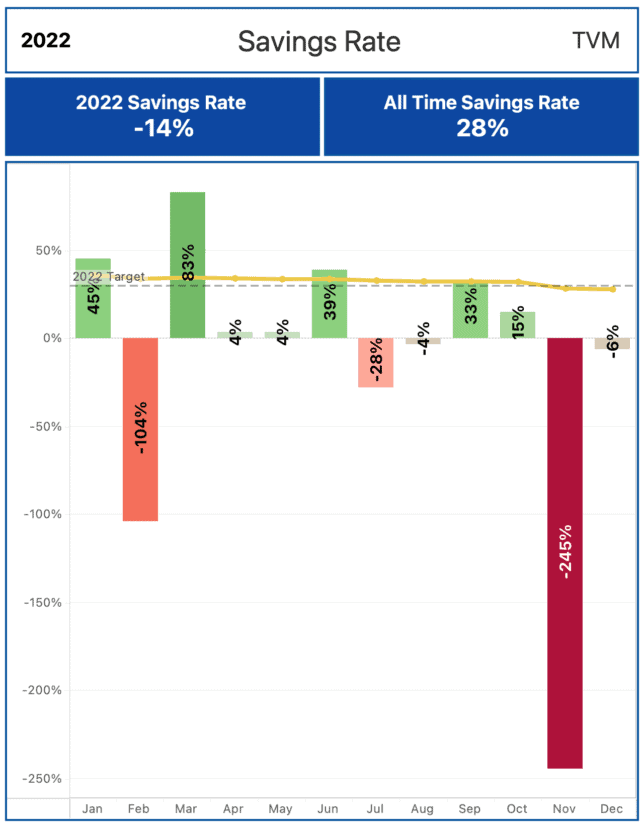

Savings Rate

Our final 2022 savings rate was -14%.

In other words, we spent 14% more than the income that we brought in.

From a pure financial independence perspective, this is absolutely terrible. There is no sugarcoating that.

Our savings rate in 2022 took a major hit due to:

- Transitioning to a single income household

- Knocking out major (some unavoidable) house projects

Because our savings rate is one of the most important metrics in achieving financial independence, our major focus for 2023 will be getting our savings rate back up to “FI Levels.” By “FI Levels” I mean consistently trying to save on average 30% or more every month.

Our plan to accomplish this is by limiting the number of house projects that we will be taking on. Furthermore, for the projects that we do decide to take on, we will be doing as much of the work ourselves as possible. Fortunately, the majority of the “necessary” projects (to keep the house running and safe)are complete. The remaining house projects on our list are more vanity in nature aka they don’t need to be done right away.

Monthly Expenses

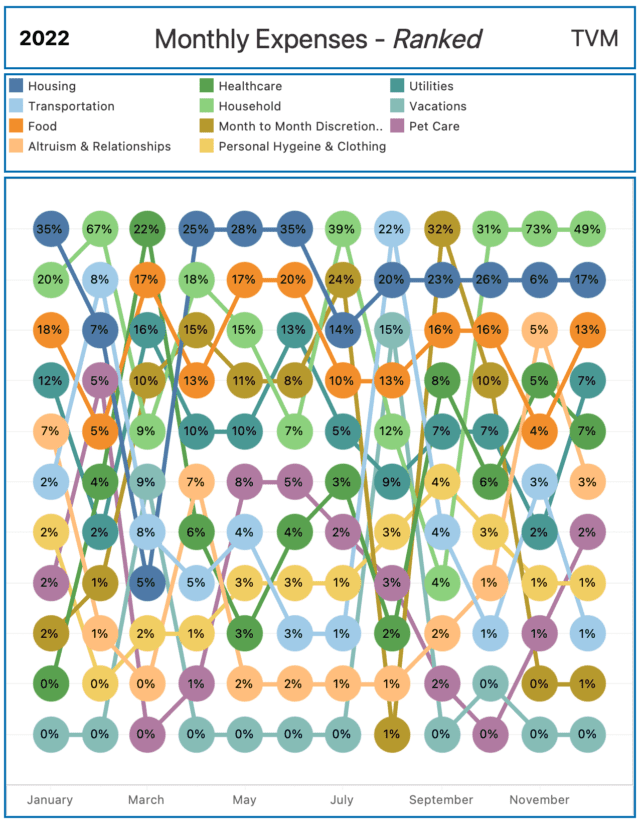

Let’s take a look at our Expense Sankey, aka Mrs. TVM’s favorite data visualization.

The above graphic visualizes how our monthly expenses rank month over month. The percentages in the individual bubbles represent our % spending for each category for that month.

Here are the major spending highlights from Q4:

- October

- Healthcare: After two years, it finally happened… our whole house got COVID. So our healthcare costs jumped due to the doctor appointments and medicine associated with that.

- Household: We made several large principal payments on our AC loan. We also paid a plumber to remove some nonfunctional pipes that were on the side of our house prior to getting our brand new siding installed.

- Month to Month Discretional: Hamilton Tickets 🙂

- November

- Healthcare: Mrs. TVM does a lot of her annual appointments in November, so just doctor appointments and expenses associated with that.

- Transportation: We had to pay for a new sensor for my car that was needed in order to lock the vehicle. If I tried to lock the vehicle… the alarm would go off. So that was fun… NOT.

- Household: WE MADE OUR FINAL SIDING PAYMENT (it hurt seeing that much money leaving our bank account at once). This included fixing all the water damage associated with the old siding. Furthermore, we made a couple more large principal payments on our AC loan as well as got a new microwave (our old one broke).

- Altruism: We made an annual contribution to our child’s UGMA Account.

- December

- Household: We had brand new seamless gutters installed (previously didn’t have gutters for a large portion of the house). We also had a few trees removed that were planted way too close to the house. We made another large principal AC payment. Furthermore, we also had an emergency with our main sewer line that needed to be fixed ASAP (no way around that one).

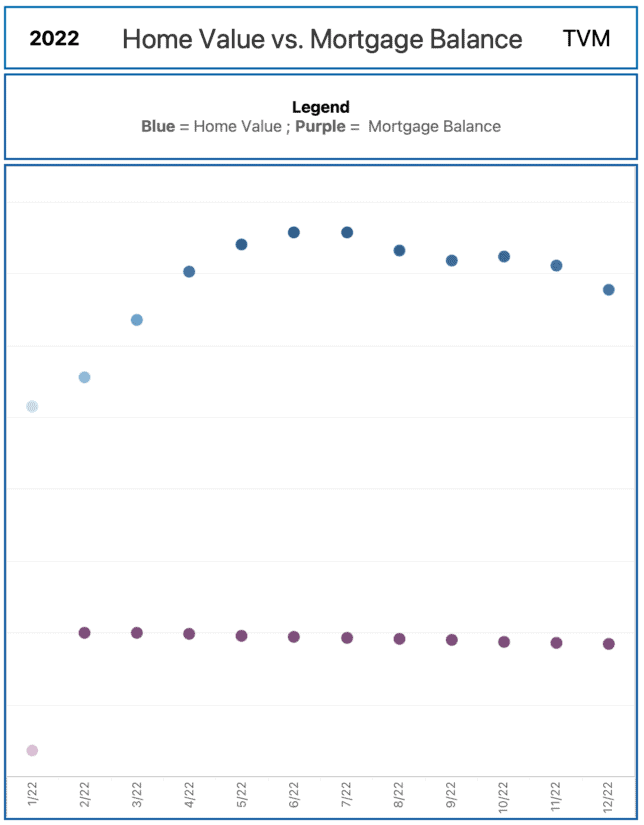

Home Value vs. Mortgage Balance

From Q3 2022 to Q4 2022, our home value decreased 2.5%.

However, our house’s value increased by a total of 11.9% in 2022.

I would argue our house’s value should be significantly higher due to the money that we’ve invested into it. However, Zillow doesn’t seem to think so 😛

Based on our home’s desirable location, we do expect the house to continue to appreciate in 2023. With that being said, it likely won’t be nearly as much as what we saw in 2021 and 2022.

Overall, we are happy that the value of the home at least kept up with inflation.

2023 Plans

I’m really looking forward to what 2023 will bring.

My goals for this next year include:

- Continue being a present father and husband by prioritizing family time

- Continue publishing articles for Time Value Millionaire and Tropical Tree Guide

- Transition to a more plant-based diet

- Becoming a certified UF Master Gardener

- A positive savings rate!

Final Thoughts

It’s important to reflect on how we have grown both financially and in our lives.

I hope that you had a great 2022 and have even better 2023 🙂

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.

Wow, what a year for you guys. You will look back much much later and ask “How the heck did we get through that?”. Ha ha.

We are in the opposite side of where you are. Kids are out, so done with home projects, etc. We are moving to an apartment and listing our house in a couple of weeks. After 23 years of home ownership we are taking a year off to figure out if we want to stay in apartment, buy condo, or buy much smaller home. We are in the paring down stage of our lives. Our current house is just too big for the two of us.

Life is constantly changing and gotta roll with with it. Good luck with 2023!

We ask that question everyday. While it’s a lot, we try our best to make sure we don’t blink and miss all the fun parts 🙂

I hear you about the downsizing. The bigger the living space, the more maintenance (cleaning, fixing things, etc.). I’m sure y’all are like “Been There, Done That” and are trying to minimize the time spent in retirement on that kind of stuff. I don’t blame you!

What do they say ? Change is the only thing that remains constant? 🙂

We also wish you the best of luck in 2023!