Welcome to the third TVM Financial Update of 2023.

The purpose of these quarterly financial updates is to crunch the numbers, visualize the data and share our progress towards becoming financially independent.

Let’s dive in!

Life Update

In the last 90 days…

I finished my Master Gardener Certification! After 11 weeks of training and 80 hours of volunteering, I am finally a Master Gardener! For those unfamiliar with the program, it offers intensive horticultural training and opportunities to share that knowledge with your community. While I wouldn’t classify myself as a true ‘master’ just yet, I did learn some valuable information that I’m excited to apply to my fall garden.

We’ve been taking advantage of the cooler weather. I love Florida, but it’s tough to do outdoor activities during the summer, especially with a baby. Now that things are cooling off, we’ve been taking the baby to the zoo (they adore the otters) and attending fall festivals in our community 🙂 I also had the opportunity to visit my best friend in Tampa and go fishing, though we didn’t catch any lunkers, I did enjoy some sea grapes!

I’ve been grinding on my other website. You may have noticed that I haven’t been publishing a lot of new content recently. Don’t worry—the website will continue to live on! While I enjoy writing about finance, I’ve been exploring other creative outlets to manage burnout and keep my mind sharp with a different writing style and audience.

Now on to the moolah!

Financial Update

A quick note: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.

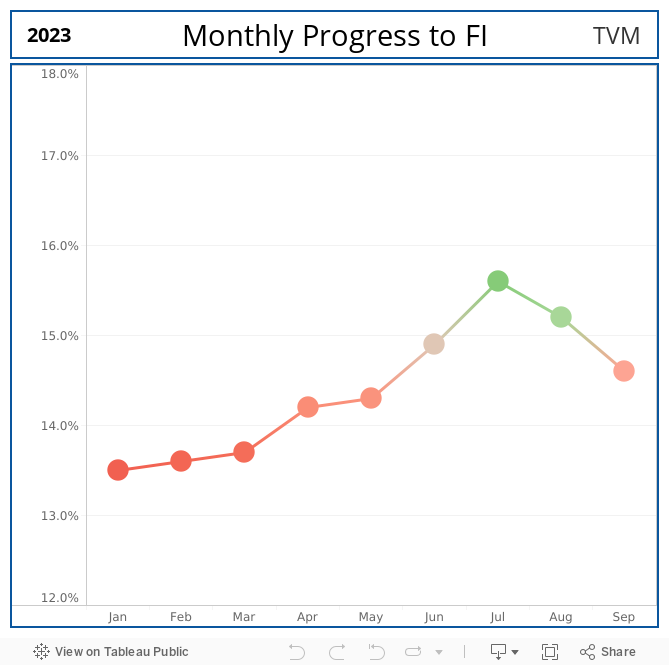

Progress to Financial Independence

From Q2 2023 to Q3 2023, our % FI decreased 0.3% from 14.9% to 14.6%.

As a reminder, our % FI is a function of two variables:

- Our average monthly spending

- The total balance of our FI Assets

In regards to our spending, we had a few unexpected emergency expenses that affected our savings rate. For more details, check out the ‘Savings Rate’ section. On the other hand, we continued saving/investing via a dollar-cost averaging strategy (business as usual).

Now, let’s delve into the specifics of our FI assets.

Asset Breakdown

The above table is a breakdown of our current FI Assets.

Although our 401(k) is our largest investment account, 58% of this year’s gains have come from pure savings, and 42% from compound interest. It’s a powerful reminder of the value of consistent saving, even with higher balances. Barring any significant market shifts, our 401(k) should yield a positive double-digit return for the year.

Our HSA is performing well, despite a fair share of medical expenses. We’re currently paying those bills out of pocket to let the investment balance continue snowballing through compound interest.

As for the Roth IRA, it’s a running joke at this point that I have been too lazy to switch from REIT-focused investments to VTSAX. Rest assured, I’ll make the change… eventually 🙂

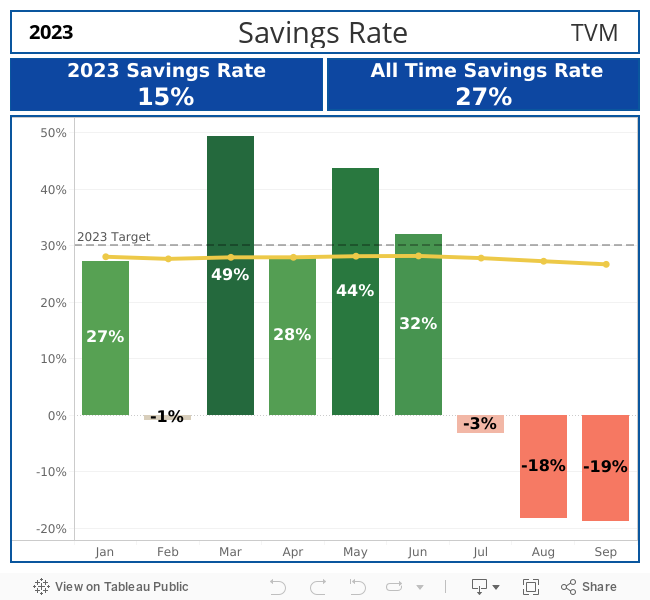

Savings Rate

Our 2023 savings rate is currently at 15%.

Unfortunately, this marks a 50% reduction from the 30% annual savings rate we reported in the Q2 Financial Update. Life threw us some unexpected expenses in Q3, but it wasn’t all bad news. We managed to pay off our AC loan! See below for more details.

Monthly Expenses

Let’s take a look at our Expense Sankey, aka Mrs. TVM’s favorite data visualization.

The above graphic visualizes how our monthly expenses rank month over month. The percentages in the individual bubbles represent our % spending for each category for that month.

Here are some of the major spending highlights from this quarter:

- July

- Healthcare: We had a slight increase in spending due to a few appointments and paying off those pesky medical bills that take months to show up 🙂

- Transportation & Travel: We had another small increase in spending as we switched to a new auto insurance provider and had to pay for the first month’s premium.

- Household: I finally completed a landscaping project that took me several months to do (it’s too hot to do everything at once). Other than that, our dryer broke (right after a mega load of laundry, no less), so we had to shell out a few galleons for that.

- Vacations: The bill for our hotel stay during our last vacation came in—ouch!

- August

- Healthcare: Had a few emergency appointments… oh the joys of getting old.

- Transportation & Travel: Our 6 month insurance premium was due with our new auto insurance provider. While it always sucks cutting a check, switching to the new provider decreased our premium by around 600 bucks, FOR THE EXACT SAME COVERAGE. Moral of the story: Always make sure to shop around!

- Household: We used savings and an extra August paycheck to pay down our AC loan.

- Pet Care: We bought a year supply of medication (flea/tick/heartworm) for the TVM Pup.

- September

- Healthcare: I had to go to the emergency room. I won’t go into details, but in case you were wondering, a 30-minute visit for an X-ray and blood sample cost $4,000. The kicker is, I left feeling worse than when I got there. Gotta love our healthcare system!

- Household: We used a chunk from our emergency fund to finally pay off that dreaded AC loan with its 15% interest rate! But, wouldn’t you know it, our AC system then developed a clogged drain and stopped working, costing us $400 to fix. You can’t make up this level of irony 😛

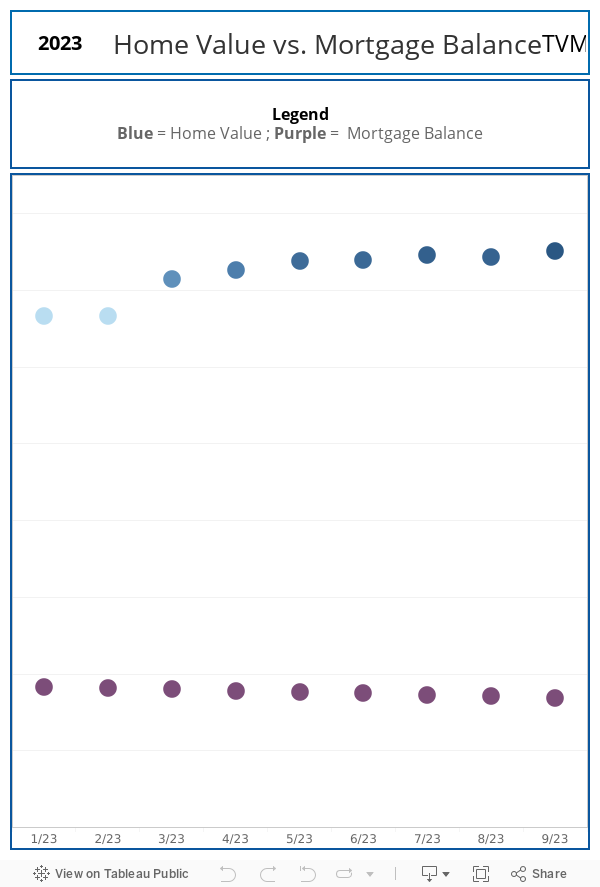

Home Value vs. Mortgage Balance

From Q2 2023 to Q3 2023, our home value increased 1.6%.

Even though we’ve finally paid off our AC Loan, we’ve temporarily paused any and all major house projects. We might tackle a few small, budget-friendly landscaping projects with the cooler weather, but that’s it!

Final Thoughts

Other than a trip to the ER and paying off our AC loan, the last three months have been pretty stable, both personally and financially.

While it was nice to finally get rid of that AC loan, our main goal now is to rebuild our emergency fund. Barring any unforeseen emergency expenses (there’s always something), we will now be laser-focused on maximizing our savings rate for the last few months of the year.

Given how much “unplanned spending” we’ve had, it’s really opened our eyes to the need for having a larger financial cushion.

In fact, we are now aiming to save 200% more than our usual earmarked amount. It will be a substantial amount of money on hand (though it will be in a high-yield savings account), but after the year we’ve had, I’ve certainly become more open to the idea of having a larger fund.

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.

Leave a Reply