When it comes to pursuing financial independence, I like to keep things simple.

Simplicity in this case is knowing the difference between needs and wants in life and having our budget reflect that.

Mastering this basic concept is one of the most effective things we can do in order to speed up our road to financial independence.

With that being said, this post will cover:

- What are Needs and Wants in Life?

- Examples of Wants and Needs

- Building a Budget for Needs and Wants in Life

Let’s dive in.

Affiliate Disclosure: Personal Capital Advisors Corporation (“PCAC”) compensates TimeValueMillionaire.com for new leads. TimeValueMillionaire.com is not an investment client of PCAC.

What are Needs and Wants in Life?

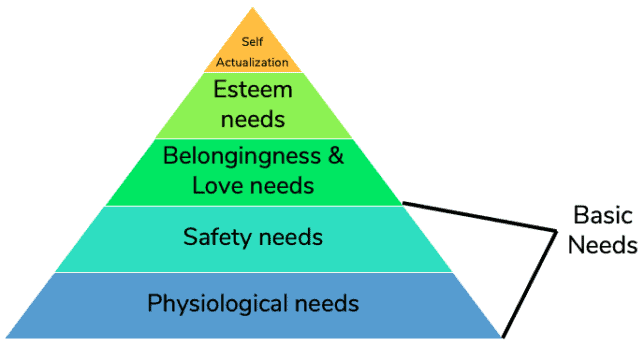

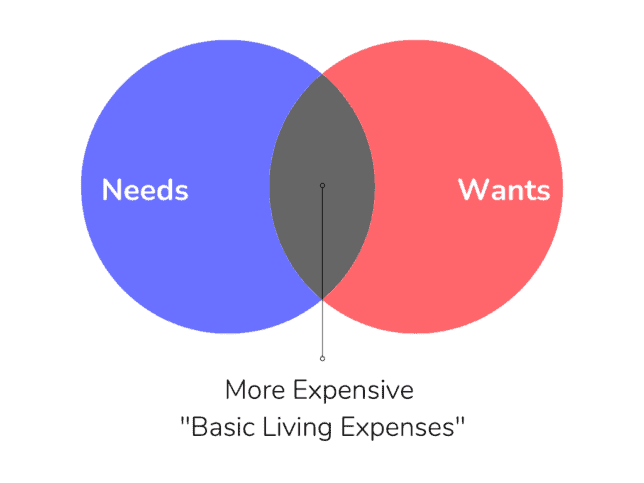

A need refers to something required for survival.

In other words, anything in the bottom two levels of Maslow’s Hierarchy of Needs:

A want on the other hand refers to something non-essential for survival, but desired to improve one’s quality of life.

With this in mind, let’s start defining different budget examples of wants and needs.

Examples of Wants and Needs

Examples of Needs

Using our definition from earlier, there are only a few basic living expenses that meet the strict definition of a need.

This includes but is not limited to:

- Food*

- Shelter*

- Clothing*

- Healthcare & Insurance*

- Personal Care Products*

Why did I include an asterisk on each category?

Because when identifying and budgeting our needs, we may attempt to pass off a want as a need.

In other words:

- Food at an expensive restaurant is technically food, but is not a need

- A mansion is technically shelter, but is not a need

- Gucci clothing is technically clothing, but is not a need

If we are not honest with ourselves, we may be inflating what our basic living expenses actually are.

This will do more harm than good.

Inflating our basic living expenses can impact almost any financial goal that we set for ourselves including: paying off debt, saving more & speeding up our path to financial independence.

Examples of Wants

Wants on the other hand, are the “fun” expenses that make our lives more enjoyable.

This includes but is not limited to:

- Vacations

- Entertainment (Cable, Movies, etc.)

- Expensive Cars

- Alcohol

- Pets

Let’s set the record straight: spending money on our wants is not a bad thing.

This is contrary to the traditional mainstream advice of: “You need to cut all your wants out if you ever want to improve your financial situation.”

And while there is some truth to that, living a fulfilling life means going beyond only buying the bare essentials needed for survival. We shouldn’t feel guilty about spending money on things that will enrich our lives.

The key is having an honest conversation with ourselves to ensure there is balance between our needs and wants in life.

Building a Budget for Needs and Wants in Life

Developing Our Need Budget (Priority)

Developing our need budget requires a degree of humility.

It requires us to objectively analyze our budget to understand how much money is needed in order to cover our basic living expenses. With that being said, what % of our budget should be allocated to our needs?

While everyone’s situation is different, a good target to strive for is 50% of our after-tax income.

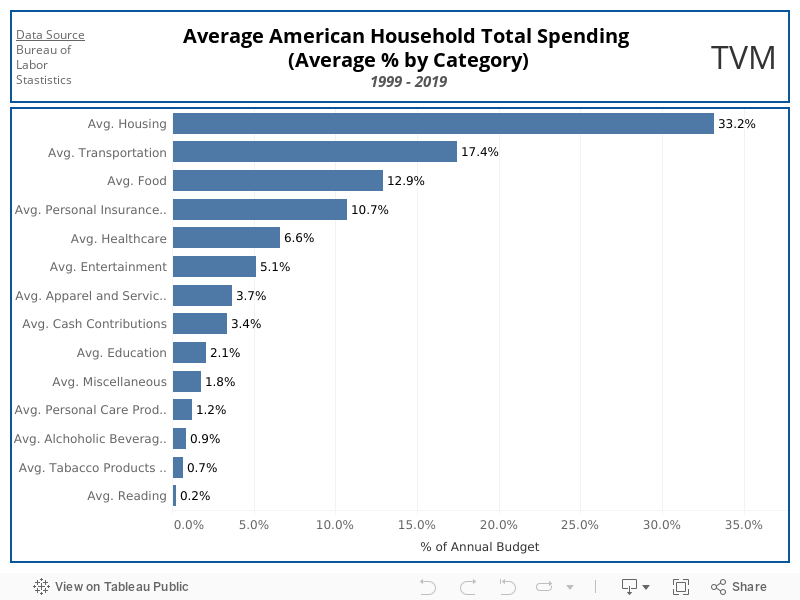

If our need budget exceeds 50% of our after-tax income, we need to evaluate how we can decrease our basic expenses. One of the most effective ways to do so is by analyzing our big 3 expenses.

As the name implies, the big 3 expenses (housing, food & transportation) make up 63.5% of the average American household’s spending. Making small changes to these 3 expenses alone can have a HUGE impact on lowering our need budget.

Fun Fact: A fringe benefit to developing our need budget is having the data we need to calculate our Lean FIRE Number 🙂

Developing Our Want Budget (Also Priority)

We shouldn’t feel guilty for wanting to spend money on ourselves.

That will only increase our chances of financial dysmorphia.

This is why developing our want budget should also be a priority. Nobody wants to just survive, we want to live enriching lives.

With that being said, what % of our budget should be allocated to our wants?

While this ultimately depends on the type of financial independence that we are pursuing, a good target to strive for is 30% of our after-tax income. That will enable us to save a minimum of 20% of our after-tax income each month.

Our want budget should be spent on the things that will contribute most to our happiness. Whether that be traveling, home improvements or buying fruit trees (maybe that last one is just me)… we need to maximize every dollar spent in our want budget.

When it comes to developing my own want budget, I like to keep the following in mind:

You can afford anything, but not everything.

Paula Pant, Afford Anything

Final Thoughts

Budgeting for our needs and wants in life boils down to balance.

A balanced budget enables us to live a comfortable life today while being able to save for tomorrow.

As a result, it’s important to develop an accountability system that works for us in order to maintain that balance.

For me personally, I track my spending using an excel spreadsheet as well as Personal Capital.

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.