Fat FIRE is having enough investments that can cover expenses associated with a higher standard of living than our current lifestyle.

This is due to the fact that Fat FIRE has the largest portfolio requirements relative to the other types of financial independence.

And while this does mean that Fat FIRE takes the longest to achieve, it also comes with a major benefit that the other types of FIRE do not have: the greatest amount of financial flexibility.

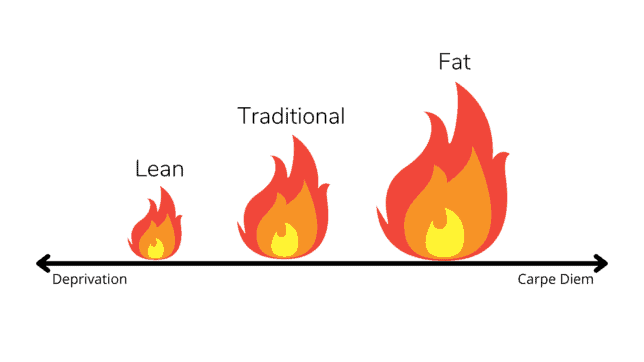

We can see this by visualizing Fat FIRE’s location on the spectrum of financial independence relative to Lean FIRE & Traditional FIRE:

Therefore if you are interested in a higher standard of living and/or additional financial security, Fat FIRE is a great goal to consider.

With that being said, this post will be looking at:

- How to calculate your Fat FIRE Number (with examples)

- The Pros and Cons of Fat FIRE

Let’s dive in.

How do you calculate your Fat FIRE Number?

Before calculating our Fat FIRE number, we first need to understand a fundamental assumption:

Everyone’s situation is different and therefore everyone’s Fat FIRE number is different.

As a result, OUR Fat FIRE number is based solely on what OUR individual expenses look like.

To say that Fat FIRE is equal to a specific annual budget amount i.e. $100,000, $200,000, etc. is saying that everyone’s situation is the same. This is simply not the case.

As an example, a $100,000 annual budget may be a Fat FIRE budget for a single individual living in Alabama but not necessarily for a family of 4 living in Hawaii.

With that being said, let’s go over step-by-step how to calculate an example Fat FIRE number.

Step 1 – Calculate our Traditional FIRE Number

The first step in order to calculate our Fat FIRE number is first calculating our Traditional FIRE number.

Our Traditional FIRE number gives us a baseline understanding of how much money is needed in order to cover the cost of our current lifestyle.

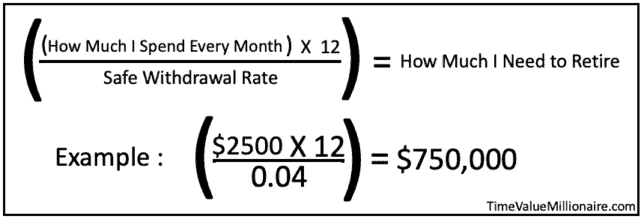

We can do this with the following formula:

Note: In this case, I am using 4% as the withdrawal rate. This is a common safe withdrawal rate to use based on research from the Trinity Study. You can adjust the withdrawal rate based on your own individual risk preferences.

However, let’s calculate an example Traditional FIRE number using real data.

According to the Bureau of Labor Statistics (BLS), the average American household’s average annual budget from 1999 – 2019 was approximately $48,278.

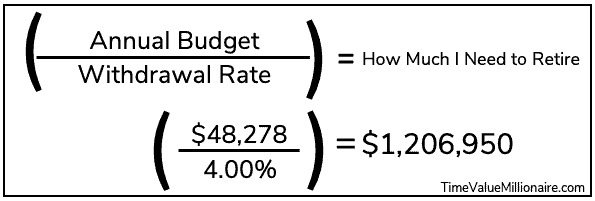

With this data, we can use the above formula in order to calculate our Traditional FIRE number:

Our Traditional FIRE number is equal to $1,206,950.

Step 2 – Calculate our Fat FIRE Number

Now that we have our Traditional FIRE number, we can calculate our Fat FIRE Number.

As a reminder, Fat FIRE refers to having enough investments that can cover expenses associated with a higher standard of living than our current lifestyle.

When looking at our example data, this would technically mean that an annual lifestyle cost of more than $48,278 / year would be considered Fat FIRE.

However, we are going to be more methodical in our approach.

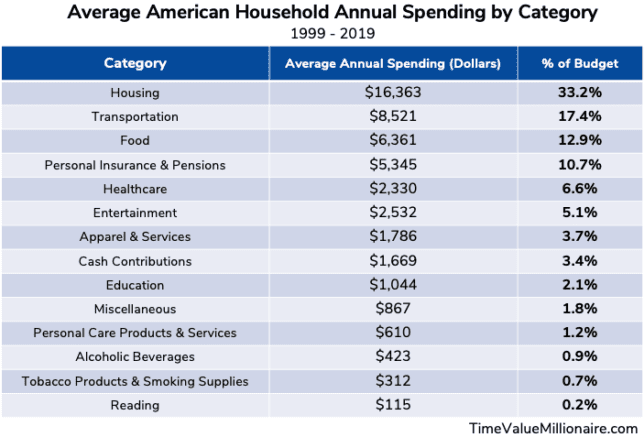

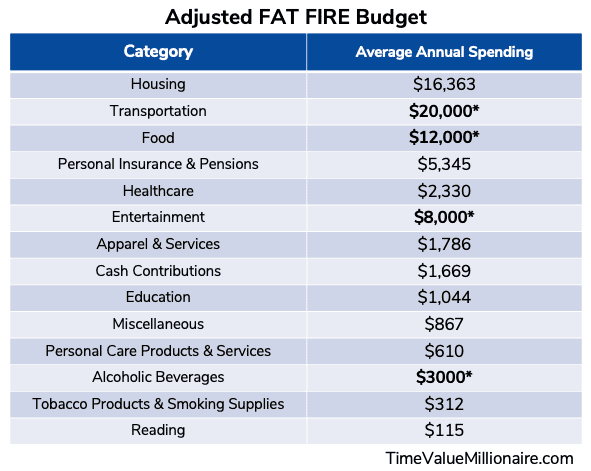

We will do this by first breaking down the BLS data into their individual spending categories:

From here, we can adjust our spending in specific categories in order to increase our standard of living.

In this case, we will define a higher standard of living as:

- Traveling more (Increase in Transportation & Entertainment)

- Eating out more (Increase in Food)

- Throwing more parties 😛 (Increase in Alcohol)

As a result, here is our new adjusted annual spending for each category:

This translates to a new adjusted annual budget of $73,441.

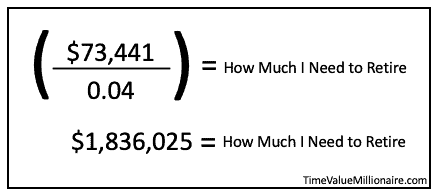

Using our FIRE formula from earlier, we can then calculate our Fat FIRE Number:

Assuming a 4% safe withdrawal rate, our new Fat FIRE number is equal to $1,836,025.

The Pros and Cons of Fat FIRE

The Pros of Fat FIRE

Fat FIRE provides a great amount of financial flexibility

The larger investment portfolio needed to Fat FIRE provides a great amount of financial flexibility.

This financial flexibility manifests itself in many different ways:

- Increased hedge against market fluctuations

- Decreased spending levels can still afford a comfortable lifestyle

- Decreased risk of losing one’s financial independence status and having to return to work

- Ability to decrease one’s safe withdrawal rate during a down market

The unparalleled financial flexibility of Fat FIRE makes it an attractive option to pursue.

Fat FIRE makes a frugal lifestyle optional

The path to financial independence requires some degree of frugality in order to save money.

However upon achieving Fat FIRE, we have the ability to make aspects of prior frugal lifestyles optional due to our savings being able to cover our increased standard of living.

So instead of worrying about cutting costs wherever possible, we can focus on enjoying the dimensions of our lives that bring us the most happiness. We can afford to live it up a little!

The Cons of Fat FIRE

Fat FIRE can facilitate lifestyle inflation

Fat FIRE enables us to have a higher standard of living.

This higher standard of living can unintentionally create a new ‘normal spending level.’

This can be dangerous for those who associate spending money with happiness, because if left unchecked can lead to lifestyle inflation mercilessly eating away at their portfolio.

Fat FIRE is not a blank check to spend as we wish. Therefore, it’s more important than ever to make sure we are following a safe withdrawal strategy.

Fat FIRE takes longer to achieve

Fat FIRE is a lot easier to do when earning 6 figures vs an average income.

Even when accounting for compound interest, achieving Fat FIRE can surely be expected to add a few more years of having to work. And if you are apart of the antiwork movement, this may be the last thing you want to do.

Therefore, if you are comfortable with your current lifestyle, don’t feel pressured to trade more years of your life in order to Fat FIRE.

Final Thoughts

I believe Fat FIRE has a bad reputation because of the context in which it’s always discussed.

Fat FIRE is not just about living a life of luxury by constantly traveling around the world or buying private submarines.

Instead, it represents having an enormous amount of financial flexibility that can substantially decrease the odds of us never having to worry about money again.

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.