According to Forbes, spending above our means was the second largest financial regret in 2022.

There is no doubt that some of this overspending can be attributed to economic conditions beyond our control such as record levels of inflation across the board as well as stagnate wage growth.

With that being said, we are ultimately responsible for our individual spending/saving habits.

As a result, today we’ll be taking a deeper look into the psychology of overspending.

Let’s dive in.

Note: I am not a medical professional, this is not medical advice.

The Definition of Overspending

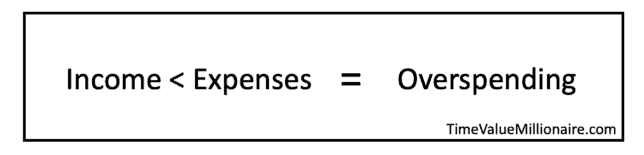

Overspending can be defined as spending more than the income that we are bringing in.

Overspending in the long term can have negative consequences on our lives such as:

- Increasing our dependency on debt

- Lowering our credit score

- Degrading our own personal financial net for emergencies

- Contributing to increased levels of stress and anxiety

- Increasing the difficulty in achieving our financial goals

Let’s now take a look at why we are overspending.

Psychology of Overspending: Identifying the Root Causes

Scarcity Principle

The scarcity principle is the economic idea that we assign a higher value to a good or service that is in low supply. By the same token, a good or service that is in high supply will have a lower value due to it’s abundance.

In the marketing and advertising world, the scarcity principle can take many different forms including advertising materials such as:

- “This widget is a limited time item!”

- “There are only X widgets left, claim yours now!”

- “This widget is on sale for a limited time only!”

Companies like eBay and QVC are very effective in maximizing the scarcity principle. The other day while on eBay, I noticed the following messaging:

- “Widget has X number of watchers”

- “Widget has X Views per hour”

- “Seller offered you and other watchers a discount, item goes to the first person to accept in the next 24 hours”

And this type of scarcity marketing is extremely effective.

Hubspot conducted a survey of 300 people to see if they were more interested in products that had a limited supply. Their survey found that “45% of respondents said that scarcity makes them want to learn more about a product.”

Between this perceived scarcity, the rise of services like “Buy Now, Pay Later,” as well as quick access to credit, it’s very easy to potentially overspend.

Lifestyle Inflation (Especially To Impress Others)

It turns out that keeping up with the Joneses is expensive.

According to a survey from LendingTree, “almost 40% of Americans have overspent to impress someone else, especially on clothes, shoes or accessories.”

LendingTree also went on to note that “more than a quarter of those who overspent to impress others are currently struggling with debt because of those purchases.”

As social animals, we are always constantly comparing ourselves to others.

One of the most common ways we do this is by comparing what material possessions that others have (cars, houses, etc.) relative to what we have. We then use other’s “perceived wealth” as the benchmark for determining what we “should have.”

The end result is overspending and engaging in lifestyle inflation in order to match this imaginary benchmark. Even if we were initially happy with what we had, we believe that we can always be happier because the “grass is greener on the other side.”

Emotional Coping Mechanism & Dopamine

Whenever we buy something that we want, we tend to feel pretty excited and good about it.

As with anything in life, retail therapy isn’t a problem when done in moderation.

This “feel good’ feeling comes from our brain releasing a hormone called dopamine, which is responsible for us feeling pleasure, satisfaction and motivation.

In the event that an individual is suffering from an issue such as depression or anxiety, shopping may provide them with a brief hit of dopamine and feel better in the short-term.

However, over time this can lead our brain to associating the act of shopping with pleasure (vs what we are buying). The end result is our brain releasing dopamine at the mere thought of shopping.

This can lead to a pattern of impulse buying and overspending in the short-term. However, this is not a sustainable long term solution when dealing with mental health issues.

In reality, we should work with a medical professional in order to identify more constructive ways to deal with any potential mental health issues that we may be experiencing.

Struggles with Delayed Gratification

At some point, you may have come across this comical video of the Marshmallow Experiment:

As we can see from the above experiment, humans can sometimes struggle with delayed gratification.

Why save for our goals when we can spend money, have our brain release dopamine and feel good now?

Neuroscientists Joseph Kable and Joseph McGuire from the University of Pennsylvania have suggested that uncertainty about the future can make delayed gratification a challenge.

“The timing of real-world events is not always so predictable… Decision-makers routinely wait for buses, job offers, weight loss, and other outcomes characterized by significant temporal uncertainty.”

Joseph W. Kable and Joseph T. McGuire

Translation: We don’t know when or if we will ever see the benefits associated with making long term decisions.

As a result, it’s easy to set aside longer term goals (financial independence, saving for a house, etc.) in order to rationalize overspending today.

Not Associating Time with Money

The price of anything is the amount of life you exchange for it.

Henry David Thoreau

Marketing and Advertising companies do an amazing job at disguising their products as the path of least resistance to happiness. Just spend X dollars on this and you WILL be happy.

As a result, why would we question how much life energy we spend? It will make us happy!

As an example, someone who makes $15 / hour and wants to buy Apple’s flagship iPhone 14 Pro Max, would have to trade approximately 107 hours or 385,200 seconds of their lives for it. Is it worth it?

We should not view our purchases in terms of money, but rather how much time that we are trading.

I would argue that we would not be as prone to overspending if we decided that being a time millionaire was more important than a dollar millionaire.

Final Thoughts

When talking about our spending habits, it’s easy for people to say: “If you are overspending, stop spending so much money.”

However, that doesn’t get down to identifying the root cause of the issue.

By having a more objective understanding of the psychology of overspending, we enable ourselves to evaluate our situations with non-judgement and come up with a plan to get us financially back on track.

Thank you for reading! 🙂

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.