Albert Einstein famously remarked that “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.”

In other words, compound interest can be a double-edged sword. While compound interest is often represented as a proven long-term road to wealth, if we are not careful, it can also take a substantial bite out of our portfolios.

As a result, today we’ll be looking at a range of fees that are common across different types of investment products. Furthermore, we will also be visualizing how paying more attention to certain investment fees can lead to us keeping more of our personal wealth in the long run.

Let’s dive in.

All Investments Have Costs

Generally speaking, there are costs associated with owning most types of investments.

Whether we are talking about ETFs or Mutual Funds, investors are often charged certain fees to cover the costs associated with owning/running a particular investment, with a few notable exceptions (Fidelity® ZERO Total Market Index Fund comes to mind).

When evaluating different investment offerings, any and all fees associated with the offering can be found in their investment prospectus. This is a legal document required by the Security and Exchange Commission that goes over all the details surrounding a particular investment.

From an investors perspective, we want to maximize our returns by minimizing the “investment friction” that we are paying in the form of investing fees. With that being said, below are 2 common different types of ongoing fees that investment products can charge us:

Expense Ratio

An expense ratio is an annual fee charged to cover an investment product’s operating expenses, expressed as a percentage of the fund’s total assets.

Expense ratios are primarily composed of marketing and management fees.

The marketing fees are also known as distribution (12B-1) fees, which are an annual charge taken from an investment’s assets to cover marketing and distribution expenses. Furthermore, there are also management fees that go to those who are actually operating the fund (i.e. investment fund manager, fund analysts, etc.).

Generally speaking, more active funds (that are trying to beat the market) will have larger expense ratios relative to more passive funds (that are trying to match the market).

Annual Account/Custodian Fees

An Annual Account/Custodian Fee is a yearly charge imposed by financial institutions for holding/managing an individual’s investments.

While this is technically an indirect cost associated with owning an investment, it is still an ongoing cost that we should be aware of and try to minimize. However, financial institutions will sometimes provide options to their customers on how they can waive these types of fees.

As an example, Vanguard will waive annual fees associated with certain investment accounts “by signing up for e-delivery of statements and the annual privacy policy notice; confirmations; reports, prospectuses, and proxy materials; and notices, amendments, and other important account updates.”

Visualizing How Fees Impact A Portfolio

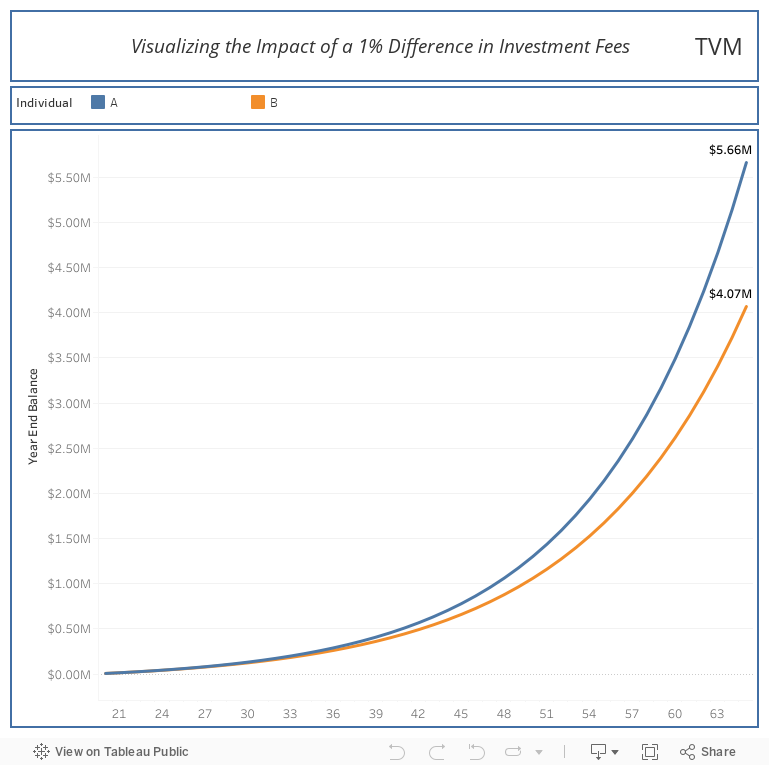

Now that have a better idea on the different types of fees that we can be charged, let’s now visualize how even a 1% fee can impact a portfolio by using the following assumptions:

| Individual A (No Fee) | Individual B (1% Fee) | |

|---|---|---|

| Age When Starting Investing | 20 | 20 |

| Retirement Age | 65 | 65 |

| Investing Contributions (2023 IRA Limit) | $6,500 / Year | $6,500 / Year |

| Gross Investment Rate of Return | 10% | 10% |

| Net Investment Rate of Return (Minus Fees) | 10% | 9% |

With our assumptions defined, let’s now take a look at the hypothetical growth of each portfolio:

Because Individual A chose an investment with 0 investment fees, Individual A’s final portfolio was 39% ($1.6M dollars) larger than Individual B’s final portfolio. While a 1% fee may seem inconsequential in the short run, the compounding effect becomes substantial in the long run.

High Fees Do Not Generate Better Returns

More often than not, we often associate higher prices with higher quality.

So investment products that boast higher fees should yield a better return right? Not necessarily. In fact, there are published studies by organizations such as Morningstar as well as S&P Global that do not support the idea of higher fees = higher returns.

Furthermore, it’s important to understand that customers are paying these fees, even if the investment’s gross rate of return is negative. By the same token, if an actively managed fund were to beat the market, they would have to do so by more than the fee that they are charging.

Going back to our example from earlier, Individual A not paying any investment fees resulted in them having $1.6M dollars more than Individual B despite saving the exact same amount of having identical gross rates of return.

Final Thoughts – Optimize Your Investing Strategy

When researching investment products that align with our specific goals and risk tolerances, we should look beyond overall returns and put a heavy (if not more important) focus on what a particular investment’s fee structure looks like.

That is because doing our homework and choosing products that minimize fees can lead to us keeping more of our hard-earned dollars and reaching financial independence a lot sooner.

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.