I can’t believe that 2020 is over. Time sure does fly by.

Today, I will be reflecting on how my life and journey to financial independence have progressed in 2020 as well as discuss my plans for 2021.

Let’s dive in!

Life Highlights

Despite all the craziness, 2020 will go down as one of the best years of my life.

In the last 365 days…

I got engaged and married the love of my life. Last January, I proposed to the now Mrs. TVM in St. Augustine, Florida underneath 3,000,000 Christmas lights. She said yes! A few months later, we had a very small ceremony and drove down to the Florida Keys for a week 🙂

Mrs. TVM and I bought a home! Two months after we got engaged, we bought a home! We didn’t plan on doing this until July, however the property was located in the area where we wanted to be and in our budget. So we jumped on it! Furthermore, I began my dream of building a suburban food forest. This year alone, we planted 13 fruit trees and 1 berry bush. We also built 6 raised beds covering 96 sqft for vegetables and spices!

We became godparents! Mrs. TVM’s sister fortunately had a healthy pregnancy/delivery before COVID-19 really picked up. They came into the world healthy and with no issues! A month later, we were asked to be their godparents 🙂

…We also became fur parents! We got a dog! We picked him up a few weeks ago and has since melted our hearts.

We spent more time with family. Since I left for college, I haven’t seen my parents as much as I would have liked. However, this year they decided to pack up and move closer to where we are at. As a result, we made it a priority to make up for that lost time together.

After four years, I finally launched TVM. I had the idea for this website since 2016, but never had the confidence to launch. However, I let go of the perfectionism that was stopping me, bit the bullet, and launched! 🙂

Financial Update

A couple notes:

- The data visualizations are interactive; hover over sections of the graphs for more detailed information.

- Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.

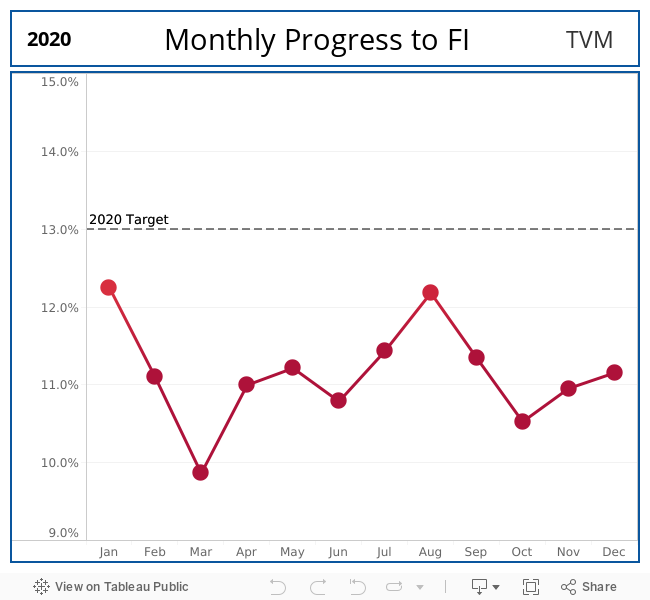

Progress to Financial Independence

Our overall % FI decreased from 12.2% to 11.2% in 2020.

Given everything that happened this year, this didn’t surprise me.

For those new to TVM, I calculate % FI via the following methodology:

- Calculate an average of what I spend every month (current month + all prior months)

- Divide by a 4% withdrawal rate to get my estimated FI number

- Divide my FI Investment Portfolio by that estimated FI number to get my % FI

Despite growing our FI Investment Portfolio (see below), we had several big expenses that increased our average monthly spending and subsequently decreased our % FI number:

- Wedding Expenses (honeymoon, venue, photographer, etc.)

- Home Ownership (down payment, necessary/unplanned renovations)

- Decreased 401(k) contributions to pay down car loans

Despite the ‘one-time’ expenses that we could probably exclude, we still see it as money spent and believe that it will average out in the long-term.

I guess that’s what happens when you decide to go full adult in one year 🙂

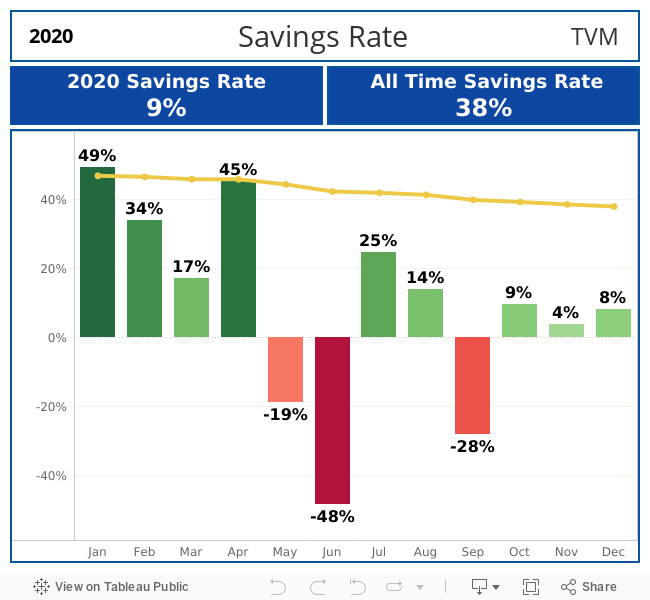

Savings Rate

Our average savings rate for 2020 was 9%.

This is a 29% decrease from my cumulative all-time savings rate of 38%.

As previously mentioned, the top three drivers for the lower savings rate were:

- Wedding Expenses (honeymoon, venue, photographer, etc.)

- Home Ownership (down payment, necessary/unplanned renovations)

- Decreased 401(k) contributions to pay down car loans

Fortunately, we do not plan on getting married again or buying another home next year.

There will maintenance associated with the home, but don’t anticipate it being more then what we spent in 2020.

Regarding the car loan, we are shooting for it to be paid off in the first half of 2021. At this point, we expect our savings rate to bounce back to normal levels.

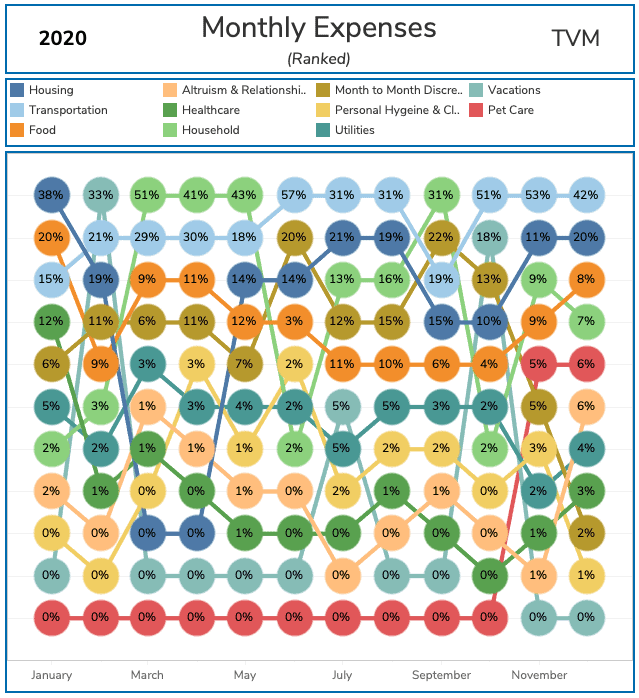

Monthly Expenses

The above graph visualizes how our monthly expenses rank month over month. The percentages in the individual bubbles represent what percentage of our income was spent on that category for that month.

Here is what immediately popped out to me:

- Spending on household (supplies, interior decorations) was the highest it’s ever been in years.

- Spending on transportation was consistently greater then spending on housing (Cars > Homes)

Our increased household spending was primarily driven by a few planned/unplanned renovations. All I can say is thank goodness for emergency funds!

I also promise I don’t own a lambo. We just want to pay off the car loans ASAP.

However, Speaking of paying down debt…

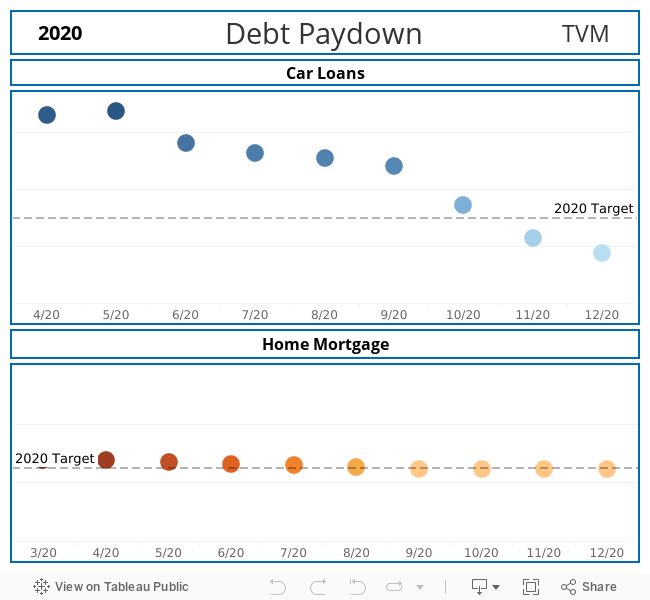

Debt Paydown

We fully paid off one car way ahead of schedule! One more to go!

To say that this felt great would be an understatement.

Two years ago, I did not plan on buying another car. However, those plans changed when my old car was completely totaled in an accident in 2019. Because I didn’t have the cash on hand to buy another, I had to take out a loan.

Most importantly though, everyone walked away with no injuries.

We are shooting for a May 2021 pay off date for the remaining car loan. After this debt is gone, we will be funneling that cash back into our retirement accounts. At that point we will have no consumer debt 🙂

For our mortgage, we met our goal! We don’t have any immediate plans to make additional principal payments. However, we will potentially be refinancing to a 15 year mortgage next year if interest rates keep going down.

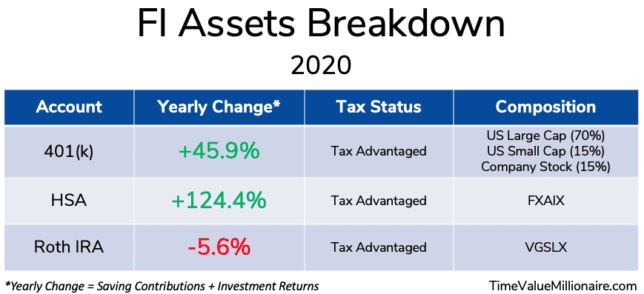

Despite the abysmal 9% savings rate, our FI Investment Accounts grew by a combined 164.7%.

This freaking blew my mind.

From a contribution perspective:

- I contributed the max amount allowed for an HSA

- I made enough contributions to my 401(k) to fully receive my employers match (aka free money)

- I didn’t make any contributions to my Roth IRA

Once the remaining car loan is paid off, we will upping our 401(k) contributions back up to pre-car loan levels. This will be critical in increasing our savings rate in 2021 and continue growing these accounts.

2021 Plans & Final Thoughts

Life Plans

In 2021, I will be simplifying my life.

I plan to narrow my focus down to practicing four habits, daily and consistently:

- Reading

- Writing

- Meditating

- Exercising

In addition to implementing these habits, my main goal for 2021 is to consistently publish new content and grow this website.

Financial Plans

Financially, my plans are:

- $0.00 consumer debt by May 2021

- 30% yearly savings rate (average)

- 15% FI

Final Thoughts

It’s easy to get caught up in noise.

However, it’s important to take a moment to reflect on how we have grown both in our lives and financially.

Goodbye 2020, Hello 2021.

Thank you for reading! 🙂

_

Full Disclosure: Nothing on this site should ever be considered advice, research or an invitation to buy or sell securities, please see my ‘Terms & Conditions’ page for a full disclaimer.